Introduction

Education, a crucial component of public services and the national economy is a task of paramount importance for the state. In Poland, financing educational tasks has been a shared responsibility between the local government and the state since 1996. This hybrid model sees a significant portion of the state’s expenditure in this area being transferred to municipal budgets through the educational part of the general subsidy and targeted subsidies.

In the light of applicable law, public education is one of the commune’s obligatory tasks, which it carries out on its behalf and under its responsibility, financing it from its budget. The educational tasks of municipalities are specified in the Education Law and include education, upbringing and care, and social prevention. Local governments are primarily responsible for establishing and running public schools and educational institutions (including kindergartens) and transporting children to schools. Their tasks and competencies in this area include material conditions, personnel and administrative matters, organisation of education and care, financial issues, substantive supervision, and organisation and administration of the network of schools and facilities (Sekuła and Nucińska, 2021).

As local governments carry out their assigned tasks, they manage substantial resources, including property, finances, and human capital. These resources should be utilised judiciously in the public interest. The qualitative nature of public goals and the limited scope for market solutions do not absolve local authorities from adhering to the principles of competitiveness and efficiency. According to Skica (2012), an increasing number of local government units view efficiency as a synonym for the quality of public administration and the rationality of public funds management. It has transitioned from being a mere assessment tool to a decisive factor in shaping the nature and directions of municipalities’ financial management.

Taking the above into account, the article aimed to assess the efficiency of rural communes’ expenditure on educational tasks and create a typology of communes related to this issue.

The Efficiency of Education Financing in the light of a Literature Review

Efficiency is a crucial concept to understand in the context of education financing. It is usually defined as the relationship between effects and the resources used to achieve these effects (Charłampowicz and Mańkowski, 2020). The basics of the theory of economic efficiency were formulated by the Italian economist V. Pareto, who claimed that the conditions of efficiency are met when the utility of one entity (object) cannot be increased without reducing the utility of another (Kucharski, 2014). In this approach, efficiency most often refers to the principle of rational management, which is formulated in two variants: efficiency (assuming obtaining the maximum effect from a given level of expenditure) and economy (meaning obtaining specific effects with the least possible expenditure) (Rutkowska, 2020). In the case of a local government unit, total efficiency is achieved when none of the inputs involved and the achieved effects can be improved without simultaneous deterioration of other inputs or effects (Skica, 2012; Kozuń-Cieślak, 2011a).

There is extensive literature on efficiency in education and related issues, comprehensively analysed, among others, by De Witte and López-Torres (2017) and Johnes (2015). Drawing on different theoretical foundations and computational methods, most authors share the common idea that education can be viewed as the result of a production process that uses variables related to students, family, school, and community characteristics as production inputs (Chiariello et al., 2022). In Poland, a review of research on the efficiency and productivity of education (primary and secondary schools) was conducted by Brzezicki (2023). His analysis shows that estimating the efficiency of education was embedded in the context of teachers’ professional advancement, the level of development and/or size of local government, the level of public funds spending, the nature of the educational process, comparative analysis of various types of schools, the sensitivity of rankings to changes in the adopted variables, benchmarks and determining optimal values.

The issue of educational efficiency can be considered in two ways, i.e., the efficiency of implementing educational tasks (which is related to the organisation of the system for providing these services) and the efficiency of financing education (which concerns the scale, methods and sources of financing). In the first case, it is about the efficiency and quality of the achieved educational effects compared to the expected ones. In contrast, the second concerns the level of financing and the principles of allocating funds for educational purposes compared to the quantity and quality of effects (Nucińska, 2017). According to Waluś (2018), the efficiency of financing educational tasks in the public sector means the degree of implementation of educational goals, which manifests itself in the maximisation of educational results and, consequently, determines the value of the state in the international arena.

When allocating financial resources, local government authorities should take into account three types of efficiency: technological (i.e. the efficiency of technology in transforming inputs into results), financial (i.e. providing goods and services of a given quality at the lowest cost), allocative (i.e. providing the optimal, in the opinion of society, combination of goods and services) (Guzik, 2009; Filipiak, 2012). They can also consider efficiency, taking into account the time horizon, focusing on dynamic efficiency (related to the ability to grow and develop in the long term) or static efficiency (related to avoiding the waste of resources constant in a given period and their best allocation) (Kozuń-Cieślak, 2013; Gerlach and Gil, 2018).

As Kozuń-Cieślak (2011b) points out, the theory of efficiency in relation to public sector entities is a complex and controversial field. Economic factors only partially determine the decisions made, and the specificity of this sector and the mission of its entities further complicate matters. The influence of the political factor, the nature of public goods, and the socio-economic premises all play significant roles. The areas in which public expenditure is incurred are generally not amenable to precise measurement of their economic and social effects, and the expenditure necessary to obtain the desired effect is often ambiguous and difficult to isolate and quantify. The problem with measuring the level of public sector efficiency also stems from the lack of a theoretically justified model level of goods and services provided by the public sector that could be considered 100% efficient at a given level of public expenditure (Kozuń-Cieślak, 2011a).

The above does not discourage researchers from looking for measurement methods. Huguenin (2015), citing Johnes (2004), distinguishes two basic approaches to measuring the efficiency of education: statistical and non-statistical. The statistical approach uses econometric techniques, while the non-statistical approach uses linear programming or mathematical algorithms. Both statistical and non-statistical approaches can be parametric or non-parametric. Parametric methods are used for models with a precisely defined structure that can be identified. They require making assumptions about the form of the production function, which determines the relationship between inputs and results and gives an answer to the question of what maximum product can be obtained with given inputs. However, it is sometimes impossible to correctly construct a satisfactory model and determine structural parameters adequate for analysis. There may also be difficulties in interpreting the obtained results. In such a situation, non-parametric methods have more excellent application value. They use mathematical (linear) programming and provide the opportunity to test the efficiency of objects that transform multiple inputs into multiple outputs. They are characterised by no need to make assumptions about the functional relationship between input and output variables. They are based on examining the relationship of the effects a given entity achieves to the “absolute standard”, i.e., the maximum, highest, possible effect specified for given conditions. Additionally, they do not require taking into account the influence of a random factor or measurement errors (Czyż-Gwiazda, 2013; Lisowski, 2014; Bartoszewicz and Lelusz, 2016; Sekuła and Julkowski, 2017).

Material and Methods

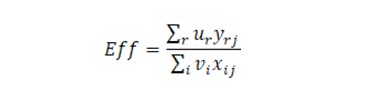

The efficiency of rural communes’ expenditure on educational tasks was evaluated using non-parametric, input-oriented, Data Envelopment Analysis (DEA). It is a widely utilized mathematical programming technique for assessing the relative efficiency of a set of homogeneous Decision-Making Units (DMUs), in this case, municipalities, which consume the same inputs (in varying quantities) to produce the same outputs (in varying quantities) (Benítez et al., 2021). In the CCR model used in this research, the efficiency score of each unit (Eff) can be represented as a ratio of the total weighted outputs to the total weighted inputs (Pedraja-Chaparro et al., 2005), according to the formula below (Mardani et al., 2017):

where: yrj – the amount of the rth output from DMUj, ur – the weight given to the rth output, xij – the amount of the ith input used by DMUj, vi – the weight given to the ith input.

All DMUs scoring Eff = 1 are deemed efficient relative to other observations, whereas DMUs with Eff < 1 are considered inefficient. A coefficient of less than one signifies instances where other municipalities achieve the task with fewer inputs (Charnes et al., 1978). When employing this technique, it is crucial to recognize the relative nature of the results, meaning that the efficiency of a selected entity is measured against the group encompassed by the study. An inefficient DMU may be erroneously evaluated as efficient due to the poorer performance of other entities.

Assessment of the efficiency of rural communes’ budget expenditures in a non-parametric approach required a set of indicators representing both inputs and outputs of educational activities. In this research, the variables representing inputs include main budget expenditures grouped in division 801 Education, i.e.:

- the sum of current expenditure on wages and salaries and expenditure resulting from wages and salaries (I1),

- current expenditure on purchase of materials and services (I2),

- other current expenditure (I3),

- property expenditure (I4).

On the other hand, the outcome side includes:

- number of pupils in schools (total in all types of schools) (O1),

- number of sections in schools (total in all types of schools) (O2),

- number of children in nursery schools (total in all types of units) (O3),

- number of sections in nursery schools (total in all types of units) (O4),

- full and part-time employed teachers expressed in terms of full-time employees in schools (total in all types of schools) (O5),

- full and part-time employed teachers expressed in terms of full-time employees in pre-primary education (total in all types of units) (O6).

All the necessary calculations were made in deaR-Shiny, credited by Benítez et al. (2021).

The k-means method was used to divide the population of rural communes into disjoint, internally homogeneous, clusters. It is an optimisation-iterative, non-hierarchical, method in which the number of clusters is assumed a priori. The computational procedure aims to distribute objects between groups so that the intra-group variability is as minimal as possible and the between-group variability is as large as possible. The F significance test is utilised to analyse variance and evaluate this condition (Stanisz, 2007). The k-means method is used to analyse large amounts of data, and its essence is to reduce a large amount of accumulated information to a few basic categories, which allows for easy orientation in a given phenomenon and drawing generalisation conclusions. The use of the k-means method makes it possible to establish a typology of the studied objects and to define homogeneous objects of analysis, in which it is easier to isolate systematic factors and possible cause-and-effect relationships (Pietrzykowski and Kobus, 2006). All the necessary calculations were made in Statistica 13.3 from TIBCO Software Inc.

Research Results

In 2012-2022, rural communes in Poland allocated, on average, 32.6% of total expenditure on educational tasks, i.e. 7.11 mln PLN (USD 1.79 mln). Over the eleven analyzed years, the nominal increase in this amount by 73.2% was accompanied by a decrease in its share in total expenditure by 11.5 percentage points. On the one hand, it was caused by the systematically increasing costs of implementing educational tasks (including teachers’ salaries and the ongoing maintenance of educational infrastructure), and, on the other hand, the reform of the education system, as a result of which gymnasiums were abolished, and primary education was shortened by one year.

Expenditures incurred by communes on educational tasks, in addition to ensuring ongoing continuity of their implementation, also include investment activities to improve the conditions in which children and youth are educated. In 2012-2022, these expenditures amounted, on average, to 4.3% of the total funds allocated to educational tasks, and the number of municipalities not undertaking this type of activities ranged from 227 (in 2014) to 407 (in 2019). The commune of Manowo (West Pomeranian Voivodeship) came first in this group. Being the managing body for three primary schools, it did not report this type of expenditure during the analyzed period. In turn, the highest amount of capital expenditure was recorded in the Kobierzyce commune (Lower Silesian Voivodeship), which spent over PLN 179 mln (USD 45.4 mln) on investments in education. These funds were allocated primarily to the modernization and expansion of existing buildings and the construction of new schools. A wide range of investment activities was the commune’s response to the systematic increase in the number of inhabitants (over the 11 years covered by the analysis, it increased by 37.9%), the number of students (an increase of 97.7%) and the number of children receiving pre-school education (an increase by 135,4%).

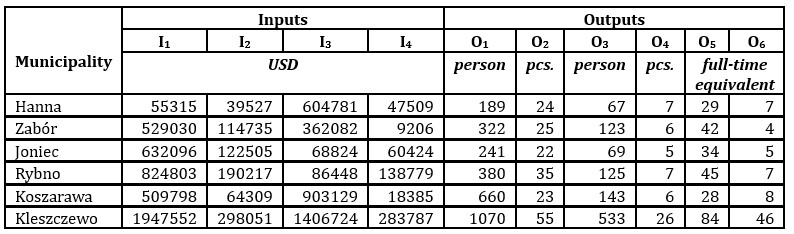

The assessment of the efficiency of rural municipalities’ budget expenditures for educational tasks was based on the results of the classic input-oriented DEA model. The calculations show that the average value of the efficiency index (Eff) in 2012-2022 was 0.8101, with the coefficient of variation ranging from 11.4% to 13.2% and the average value of the range of 0.5767. In the group of 1,513 rural communes included in the study, more than ¾ showed Eff less than one, and the set of units that were efficient in each year counted only six local governments. The communes accounted for in this group and their average inputs and output values are listed in Table 1.

Table 1: Average values of inputs and outputs (for 2012-2022) in the set of most efficiency municipalities

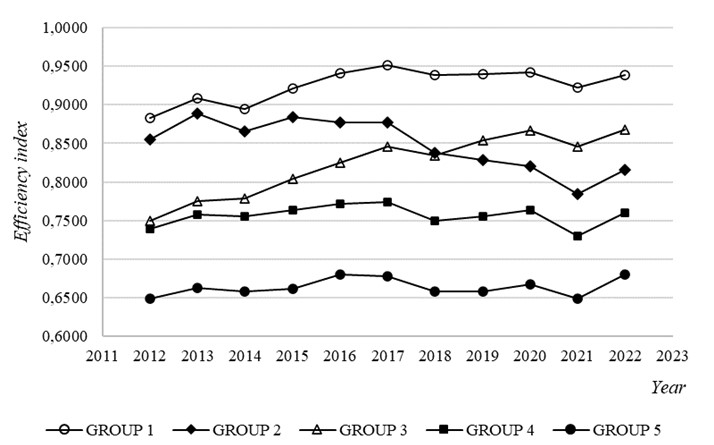

The efficiency index of the remaining 1,507 rural communes averaged for the years 2012-2022 ranged from 0.4394 in the Kleszczów commune (Łódź Voivodeship) to 0.9994 in the Rokietnica commune (Podkarpackie Voivodeship). In order to better illustrate the situation in the studied local governments, this group

was divided into five clusters using the k-means method. The primary basis for establishing the number of sets was the range of the efficiency coefficient <0-1>, facilitating the identification of interval boundaries through increments of 0.2. Average efficiency indicators for individual groups are presented in Figure 1.

Fig. 1. Average efficiency indexes for groups 1-5 (2012-2022)

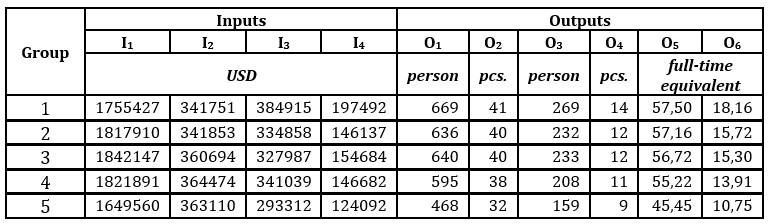

Table 2 lists the average values of inputs and outputs (for the years 2012-2022),

describing the groups identified using the k-means method.

Table 2: Average values of inputs and outputs (for 2012-2022) in groups 1-5

According to the analysis, group 1 (consisting of 269 communes) characterized the highest level of efficiency (averaging 0.9256). Compared to the remaining clusters, it stood out with the lowest current expenditure for the purchase of materials and services (I2) and relatively low (penultimate in descending order) current expenditure on wages and salaries (with expenditures resulting from wages and salaries) (I1). Because these variables accounted for over ¾ of the total inputs, the fact that the two remaining indicators (i.e. other current expenditures – I3 and property expenditure – I4) reached their maximum values did not negatively affect the final result. In turn, on the outputs side, this group was characterized by the highest values of all variables included in the study. Therefore, the achieved level of efficiency was the result of a favourable relationship between low inputs and high outputs. It should be emphasized, however, that this set was highly diversified internally, as evidenced by the highest coefficients of variation and relatively high values of ranges of almost all features included in the study.

The next cluster, group 2, consisted of 277 municipalities, which in 2012-2022 achieved an average Eff = 0.8484. On the inputs side, these communes realized current expenditure on wages and salaries (I1) and current expenditure on the purchase of materials and services (I2) on average USD 62,483.42 and USD 101.95 higher than the communes of the previous cluster. The values of the remaining two financial indicators placed the cluster in descending order in the third (I3) and fourth (I4) positions. However, when it comes to output indicators, except for O1 and O3, they achieved values that placed the group in the second place in the individual rankings. Generally speaking, this group incurred slightly higher expenses than the previous group while achieving worse results. Moreover, a decrease in the efficiency coefficient’s value took place, resulting in the described group dropping from second to third position in the final years of the analyzed period.

The third group included 351 local governments, which in 2012-2022 achieved an average efficiency index of 0.8223. The distinguishing feature of this set was the highest value of current expenditure on wages and salaries among all clusters (I1). Since this indicator accounted for more than half (68.6%) of the total expenditure allocated by this group for educational tasks, it can be assumed that it had a decisive impact on the obtained result. In turn, on the output side, most indicators had values lower than in group 2. As a result, in the rankings prepared for single variables, this cluster, except for O1 and O3, occupied the third position in descending order. The analysis of the efficiency index of this group using a dynamic approach showed that, over the years, it was characterized by an upward trend, thanks to which this group advanced to the second position in the last three years.

The penultimate set (group 4) consisted of 455 communes, which, on average in 2012-2022, achieved an efficiency level of 0.7563. Generally speaking, this result means that, to achieve the current effects, this group should use 24.4% fewer inputs. In other words, if the communes of this cluster achieved results in line with their efficient benchmarks (indicated in the DEA procedure), they would use only 75.6% of the funds they have so far allocated for educational tasks. On the expenditure side, this group was distinguished by the highest level of current expenditure on the purchase of materials and services (I2), which, after a decline in 2020, recorded an intensive increase in the next two years. As with the other four clusters, this was due to price increases due to the crisis caused by the Covid-19 pandemic and the war in Ukraine. Despite the high values of the indicator, its dynamics over the analyzed period (77.3%) can be considered moderate – the highest increase occurred in group 1 (98.3%), while the lowest in group 5 (70.9%). The remaining financial indicators placed this group in the second (I1, I3) and third (I4) positions. In this set, high budget expenditures were accompanied by relatively low outputs, placing the group in fourth place in descending order each time.

The last group consisted of 155 communes that obtained the lowest efficiency index, averaging 0.6638. Compared to the remaining sets, this cluster stood out with the second-highest current expenses for purchasing materials and services (I2) and the lowest values of other financial indicators. On the output side, the analyzed group also achieved the lowest indicators among all municipalities, each taking the last place (in descending order) in the rankings prepared for individual variables O1-O6. Compared to the remaining sets, group 5 also stood out with the lowest values of the range and coefficient of variation for all features included in the study, both on the input and output side, which proves its internal homogeneity.

The analysis showed that rural communes in Poland differ in the expenditure on educational tasks and the results achieved in this process. In 2022, the range in budget expenditure on education and upbringing per capita amounted to USD 1,312.71 – the highest value of the indicator (USD 1,565.62) was recorded in the commune of Kleszczów (Łódź Voivodeship), while the lowest (USD 252.91) was recorded in Giby (Podlaskie Voivodeship). These differences were determined by several factors, including the location of the commune, its wealth, demographic processes, and others. However, regardless of the conditions in which the local government functions, attention to the efficient spending of financial resources is crucial from the point of view of ensuring residents’ appropriate quality of life and the socio-economic development of rural areas. In conditions of permanent shortage of financial resources and the growing needs of the local community, knowledge about the efficient use of available resources and the determinants of this process is an essential element of the strategy to optimize the allocation of funds.

Conclusions

Rural communes often struggle with limited financial resources, which negatively affects the quality of educational infrastructure and the availability of teachers and, in the long run, translates into the quality of human capital in these areas. For this reason, analysing the efficiency of budget expenditure should be a primary tool for education management in every local government. Aside from optimising resource utilisation, this analysis can also help identify the best practices and solutions that can be adapted and implemented in other rural communes. By sharing knowledge and experience, communes can jointly strive to improve the implementation of tasks assigned to them by law and contribute to improving the quality of life of local communities.

The analysis carried out in this study aimed to assess the efficiency of rural municipalities’ budget expenditures on educational tasks and create a typology of communes related to this issue. It shows that the characterised set of units was quite diverse in this respect, as evidenced by the average value of the coefficient of variation at 12.4%. The most efficient group of communes was formed by six units, which achieved index Eff =1 in each year covered by the analysis. In turn, the least efficient group included 155 communes, which did not achieve such a result in any of the studied years. However, when interpreting the study results, it should be noted that reduced efficiency may be caused by various (not consistently negative) factors, including the scope of investment policy, depopulation processes and government policy. Hence, it is essential to continue research to identify the determinants of efficiency and optimise the expenditure of rural commune budgets on educational tasks.

References

- Bartoszewicz A. and Lelusz, H. (2016), ‘Idea i kierunki wykorzystania metody DEA do pomiaru efektywności działania gmin – wybrane aspekty,’ Finanse, Rynki Finansowe, Ubezpieczenia, 2(80), 217-225.

- Benítez, R., Coll-Serrano, V. and Bolós V. J. (2021), ‘deaR-Shiny: An interactiveweb app for Data Envelopment Analysis,’ Sustainability, 13(12), 6774.

- Brzezicki, Ł. (2023), ‘Przegląd badań dotyczących efektywności i produktywności oświaty (szkół podstawowych i ponadpodstawowych) w Polsce, prowadzonych za pomocą metody Data Envelopment Analysis i indeksu Malmquista,’ Entrepreneurship – Education, 19(2), 115-129.

- Charłampowicz, J. and Mańkowski, C. (2020), ‘Economic efficiency evaluation system of maritime container terminals,’ Economics and Law, 19(1): 21–32.

- Charnes, A., Cooper, W. W. and Rhodes, E. L. (1978), ‘Measuring the efficiency of decision making units,’ European Journal of Operational Research, 2(6), 429-444.

- Chiariello, V., Rotondo, F. and Scalera D. (2022), ‘Efficiency in education: primary and secondary schools in Italian regions,’ Regional Studies, 56(10), 1729-1743.

- Czyż-Gwiazda, E. (2013), ‘Koncepcje pomiaru efektywności funkcjonowania organizacji–zastosowanie metody DEA w ocenie efektywności organizacji,’ Zarządzanie i Finanse, 1(1), 103-116.

- De Witte, K. and López-Torres, L. (2017), ‘Efficiency in education: a review of literature and a way forward,’ Journal of the Operational Research Society, 68, 339-363.

- Filipiak, B. (2012), ‘Efektywność gospodarowania środkami publicznymi – uwarunkowania a rzeczywiste ograniczenia,’ Zeszyty Naukowe Uniwersytetu Szczecińskiego. Finanse, Rynki Finansowe, Ubezpieczenia, 50, 607-616.

- Gerlach, J. and Gil, M. (2018), ‘Efektywność przedsiębiorstwa w teorii ekonomii – która z definicji najlepiej oddaje istotę zagadnienia?’ Zeszyty Naukowe Uniwersytetu Szczecińskiego. Współczesne Problemy Ekonomiczne. Globalizacja. Liberalizacja. Etyka, 2(18), 13-22.

- Guzik, B. (2009), Propozycja metody szacowania efektywności instytucji non profit,’ Roczniki Ekonomiczne Kujawsko-Pomorskiej Szkoły Wyższej w Bydgoszczy, 2, 75-92.

- Huguenin, J. M. (2015), ‘Determinants of School Efficiency: The Case of Primary Schools in the State of Geneva, Switzerland,’ International Journal of Educational Management, 29(5), 539-562.

- Johnes, J. (2004), Efficiency measurement, In: Johnes, G. and Johnes, J. (Eds), International Handbook on the Economics of Education, Edward Elgar Publishing, Cheltenham, pp. 613-742.

- , J. (2015), ‘Operational research in education,’ European Journal of Operational Research, 243(3), 683-696.

- Kozuń-Cieślak, G. (2011a), ‘Wykorzystanie metody DEA do oceny efektywności w usługach sektora publicznego,’ Wiadomości Statystyczne, 3, 14-42.

- Kozuń-Cieślak, G. (2011b), Dylematy oceny efektywności podmiotów sektora publicznego w retrospekcji teoretycznej, In: T. Bernat (Ed.) Teoria i praktyka gospodarowania, Wydawnictwo PPH ZAPOL, Szczecin.

- Kozuń-Cieślak, G. (2013), ‘Efektywność – rozważania nad istotą i typologią,’ Kwartalnik Kolegium Ekonomiczno-Społecznego Studia i Prace, 4, 13-42.

- Kucharski, A. (2014), Metoda DEA w ocenie efektywności gospodarczej, Retrieved form https://docplayer.pl/42562090-Pojecie-efektywnosc-w-metodach-analizy-granicznej.html (16.02.2023).

- Lisowski, M. (2014), ‘Metoda Data Envelopment Analysis (DEA) w ocenie efektywności podmiotów,’ Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu, 343, 364-375.

- Mardani, A., Zavadskas, E. K., Streimikiene, D., Jusoh, A. and Khoshnoudi, M. (2017), ‘A comprehensive review of data envelopment analysis (DEA) approach in energy efficiency,’ Renewable and Sustainable Energy Reviews, 70, 1298-1322.

- Nucińska J. (2017), ‘Uwarunkowania pomiaru efektywności finansowania edukacji – zarys problemu,’ Progress in Economic Sciences, 4, 103-118.

- Pedraja-Chaparro, F., Salinas-Jiménez, J. and Smith, P. C. (2005), Assessing Public Sector Efficiency: Issues and Methodologies. Retrieved from https://ssrn.com/abstract=2018855 (26.03.2023).

- Pietrzykowski, R. and Kobus, P. (2006), ‘Zastosowanie modyfikacji metody k-średnich w analizie portfelowej,’ Zeszyty Naukowe Szkoły Głównej Gospodarstwa Wiejskiego. Ekonomika i Organizacja Gospodarki Żywnościowej, 60, 301-308.

- Rutkowska, A. (2020), Efektywność funkcjonowania urzędów administracji publicznej w Polsce, Wydawnictwo Uniwersytetu Warmińsko-Mazurskiego w Olsztynie.

- Sekuła, A. and Julkowski, B. (2017), ‘Zastosowanie metody DEA w ocenie efektywności wydatków jednostek samorządu terytorialnego – przegląd literaturowy wyników dotychczasowych badań w przestrzeni europejskiej,’ Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu, 477, 220-231.

- Sekuła, A. and Nucińska, J. (2021), Finansowanie zadań oświatowych jednostek samorządu terytorialnego, Instytut Badań Gospodarczych.

- Skica, T. (2012), ‘Efektywność działania jednostek samorządu terytorialnego,’ Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu, 271(2), 306-316.

- Stanisz, A. (2007), Przystępny kurs statystyki : z wykorzystaniem programu STATISTICA PL na przykładach z medycyny. Tom 3. Analizy wielowymiarowe. StatSoft Polska sp. z o.o.

- Waluś S. (2018), ‘Efektywność finansowania polskiego systemu oświaty – analiza porównawcza,’ Zeszyty Naukowe Wyższej Szkoły Humanitas. Pedagogika, 16, 89-98.

- Wojciechowski, E. (2012), ‘Ekonomiczne oblicze samorządu terytorialnego,’ Zeszyty Naukowe Wyższej Szkoły Bankowej w Poznaniu, 41, 201-210.

- Zioło, M. (2013), ‘Efekty i efektywność jako przedmiot pomiaru w sektorze publicznym a paradoks towarzyszący procesowi. Aspekty teoretyczne i metodyczne,’ Finanse Komunalne, 10, 19-32.