Introduction

Upon entering the European Union, each new Member State automatically commits to replace its national currency with the euro. The actual euro introduction date partly depends on the fulfilment of specific conditions (economic preparedness) and partly on the political will of each country.

The objective of this paper is to assess the economic and institutional preparedness for the euro introduction in the Czech Republic and specify the reasons this step has been postponed. The paper relies on the hypothesis that the preparedness for the euro introduction is sufficient. There are two reasons for rejecting the euro introduction in the Czech Republic:

Both the Government and the central bank fear the existing situation and other perspectives of the euro area as well as the obligations arising there from them.

The public is concerned about the implications of the euro adoption, particularly about rising inflation.

Therefore, the paper focuses on such concerns about inflation, examining whether or not they are justified.

The structure of the paper is as follows. The literature review is followed by a brief analysis of the reasons for rejecting the euro in the Czech Republic. The next part assesses the preparedness of the Czech economy for the euro introduction, using the nominal and the real convergence criteria to the euro area. This is followed by an evaluation of the euro adoption perspective.

The next part examines the connection between the euro adoption and the price stability and inflation in terms of both short-term and long-term effects. The subsequent section explores the relationship between the actual and the perceived inflation, applying the perceived inflation quantification method in order to deduce any dependability of both types of inflation. The last part examines experiences of economies similar to the Czech economy, i.e. Slovakia and Slovenia, deducing potential implications of the euro introduction for the Czech economy.

The Conclusion summarizes key findings of individual sections of the paper.

In order to fulfil our objectives, we have used statistical data analyses (comparison of economic data for the Czech Republic and for the euro area), opinion poll results (Eurobarometer), and comparison of the development of the actual inflation and the perceived inflation for the Czech, Slovak, and Slovenian economy.

Literature Review

Accession of the Czech Republic to the euro area has been covered by a number of authors. One of the main opponents of the euro introduction in the Czech Republic is Mach, who summed up his arguments in his book Jak vystoupit z EU (How to leave the EU). Janackova is another opponent of the euro area enlargement process, particularly in her book Peripetie ceske ekonomiky a meny aneb nedejme si vnutit euro (Peripety of the Czech economy and currency, or, let’s not have the euro forced on us). Various benefits and risks associated with the euro introduction are mainly covered in the book of Helisek et al. entitled Euro v Ceske republice z pohledu ekonomu (The euro in the Czech Republic from the perspective of economists).

Preparations for the euro introduction are mainly included in the document National Euro Changeover Plan for the Czech Republic prepared by the National Coordination Group for euro changeover in the Czech Republic. In addition to this, there are many studies that examine the preparations for the euro introduction as well as the effects thereof, particularly the Studie vliv zavedeni eura(Study of the impact of the euro adoption (Lacina et al.).

The evaluation of views of the Czech public regarding the euro introduction has been taken over from the Eurobarometer surveys (EC) and the Czech Public Opinion Research Center.

Nominal convergence (Maastricht convergence criteria) is assessed in the Convergence Report of the EC and the Convergence Report of the ECB. To supplement the aforementioned materials, the Convergence Program of the Czech Republic has been used herein. Real convergence evaluations are included in the Analyses of the Czech Republic’s Current Economic Alignment of the Czech National Bank; however, the assessment has been prepared based on the Eurostat statistical data for the purpose of the current view.

Effects of the euro introduction on inflation in the existing euro area countries were analysed in, for example, a study of the National Bank of Slovakia entitled Vplyv zavedenia eura na inflaciu v Slovenskej republike v januari 2009 (Impact of the euro introduction on inflation in the Slovak Republic in January 2009) or in the publication of Lacina, Rozmahel, Rusek 10 years of euro: success?.

Detailed analysis of the perceived inflation phenomenon and of the relation of the actual and the perceived inflation is also included in the book of Dedek Doba eura. Uspechy i nezdary spolecne evropske meny(The era of the euro. Successes and failures of the common European currency).

Rejecting the Euro

Institutional Arrangements for Introduction of the Euro (November 2005) set a “working date” for the euro introduction – i.e. 1 October 2010. On 25 October 2006, the Government of the Czech Republic decided not to attempt the accession to the exchange rate mechanism ERM II in 2007, which resulted in the annulment of the original plan to enter the euro area in 2010. The Czech Republic’s Updated Euro Area Accession Strategy (August 2007) confirmed both the annulment of the original date (2010) as well as the absence of a new specific date for the planned accession to the euro area. The annually published Assessment of the Fulfilment of the Maastricht Convergence Criteria (Ministry of Finance and the Czech National Bank) have included the same recommendation for the Government of the Czech Republic since 2006 – i.e. not to set a date for the accession to the euro area and, consequently, not to pursue the country’s accession to the exchange rate mechanism ERM II.

The Assessment of December 2014 (p. 4) says about the institutional changes in the euro area: “These changes are Fundamentals changing the conditions and obligations arising from Czech Republic’s potential membership of the euro area”. The euro area “has moved away from the situation that existed when the Czech Republic entered the EU [i.e. in 2004].” This indirectly disputes the obligation of a new Member State to sooner or later adopt the euro. This is openly described by S. Janackova (2014, p. 97): “It no longer makes any sense to talk about our “obligation” to adopt the euro in connection with the major overhaul of rules that govern the functioning of the euro area. We certainly did not undertake to enter this euro area”. P. Mach (2012, p. 62) even fears that “[…] the European Commission may decide about the membership of the Czech Republic in the euro area even against the will of the Czech Republic.”[1]

The decision not to set a specific euro area accession date is particularly substantiated as follows:

1) Changes in the euro area – new engagements

The uncertainty regarding the institutional arrangement of the euro area had previously been seen as a “major barrier” to the euro adoption. This uncertainty has declined – as a result of the establishment of the European Stability Mechanism (ESM) and also a clearer plan for establishing a banking union. However, this is associated with new costs for the euro area members. The replacement of the Czech koruna with the euro would specifically result in the following costs:

- Contribute about CZK 51 billion within four years from the accession to the euro area as a registered capital of the ESM; moreover, additional contributions of up to CZK 391 billion would need to be made in case it is necessary to promote the credit ability of the ESM (however, this is very unlikely);

The participation in the Single Supervision Mechanism (SSM, as of fall of 2014) will be associated with a fee of EUR 1.8 million to be paid to the European Central Bank by domestic credit institutions for the aforementioned supervision;

- The participation in the Single Resolution Mechanism (SRM) is associated with a contribution to the Single Resolution Fund (SRF)in the amount of CZK 17.3 billion.

2) Preparedness of the Czech Republic

The Government and the Czech National Bank state that the economic preparedness for the euro introduction has been improving. This specifically means that all the Maastricht criteria will have been fulfilled within a medium-term horizon (with the exception of our participation in ERM II – see below). In order to ensure sustainable fulfilment of the criteria, it is necessary to focus on:

- Reforms of public finance, particularly by implementing a pension reform;

- Labour market flexibility;

- Achieving higher real convergence (this implicitly means the price level convergence in particular, see below).

Nominal and Real Convergence to the Euro Area

Nominal Convergence

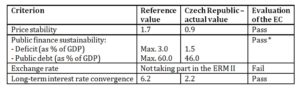

The assessment of the fulfilment of the nominal convergence criteria is performed by the European Commission and the European Central Bank every two years (or upon request of a country wishing to introduce the euro). Both institutions prepared their latest reports in June 2014. The below table no. 1 summarizes the assessment results for the Czech Republic.

Table 1: Maastricht convergence criteria (%)

Source: The processing of the authors on the basis of European Commission, 2014; European Central Bank, 2014.

Notes:

Period of assessment for the inflation and interest rate criteria = March 2013 – April 2014; for fiscal criteria = 2013; for the exchange rate criterion = May 2012 – May 2014.

* “If the Council decides to abrogate its excessive deficit procedure, the Czech Republic will fulfil the criterion on public finances” (European Commission, 2014, p. 9). This process was abrogated in June 2014.

Fulfilment of the price stability criterion and interest rate criterion can have assumed to be the same in the upcoming years. Rise of the harmonized index of consumer prices should remain stable around 2% and interest rate around 2-3%.

The public finance sustainability is also assumed within the Czech Convergence Program of April 2015. Table no. 2 contains the public finance development prognosis.

Table 2: Czech public finance development prognosis (as % of GDP)

Source: The processing of the authors on the basis of Ministry of Finance. Czech Republic.2015, p. 22.

Detailed commentary should be addressed to the exchange rate criterion. The Czech koruna does not take part in the ERM II. The reason for this is a strategy that “the Czech Republic would stay in ERM II for the minimum possible period”.

Therefore, the Czech Republic will only take part at the moment a date is set for the euro area accession. However, the fulfilment of the criterion can be simulated. For this purpose, we will assume the approach of the ECB. As a starting point, we will use a hypothetical central parity at the level of the actual average exchange rate in the first month of the period under review, i.e. May 2012 (25.3133 CZK/EUR). The development shows maximum variations:

- 5% in terms of appreciation,

- 6% in terms of depreciation.

Considering the spread of the fluctuation range, i.e. 15% both ways, this criterion can be considered fulfilled.

It’s necessary to add the following comments on this simulation of the participation of CZK in ERM II. On 7. 11. 2013, the Czech National Bank (CNB) has decided on using exchange rate intervention on the CZK/EUR rate with the goal of preventing appreciation of the rate below 27 CZK/EUR.

The effect was as follows:

- immediate depreciation from 25.83 to 26.97 CZK/EUR,

- until 20. 12. 2013 depreciation got to 27.66 CZK/EUR,

- the highest depreciation was achieved 13. 1. 2015, at 28.29 CZK/EUR,

- after which steady appreciation came into effect (without major fluctuations) to 27 CZK/EUR in late 2015.

Due to the above stated exchange rate regime with interventions, it is not possible to use the years 2014 and 2015 to simulate the participation of the Czech koruna in ERM II. However, this development states that in the timeframe before this new regime of currency rate (2012-2013), the CZK/EUR rate has not been subject to major fluctuations.

Real Convergence

In addition to the Maastricht (nominal) convergence criteria, countries adopting the euro should demonstrate sufficient level of the so-called real convergence to the euro area. It is mainly expressed via the following indicators:

- Convergence of economic level that expresses the convergence of competitiveness of converging economies. This is important since independent exchange rate policy would no longer exist that would allow the country to affect its competitiveness through its national currency;

- Convergence of price levels, which is important in terms of the development of inflation. In case of a significant difference in the price levels, there is a risk of sudden convergence of the lower price level of an acceding member to the higher price level of the euro area;

- Alignment of business cycles that comply with the single monetary policy of the monetary union’s single central bank.

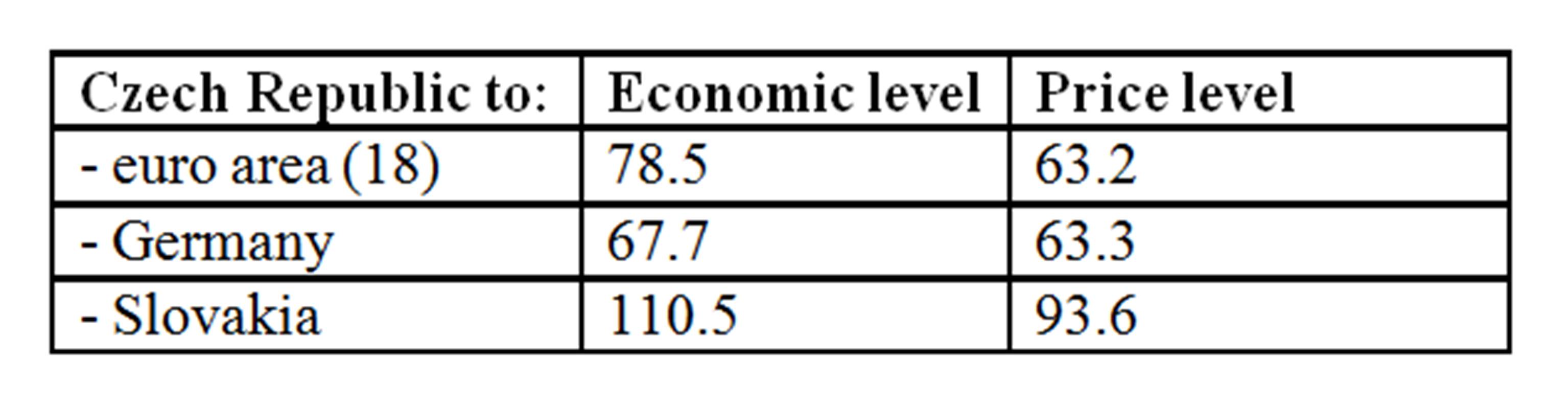

In the area of economic level, the Czech Republic got to 78.5% of the euro area (18) level in 2014. However, an indicator that compares the country’s economic level with that of its main trading partners, to which the country’s competitiveness is important, is more significant. Therefore, Table no. 3 shows this indicator in relation to Germany and Slovakia.

Table 3: Comparison of economic and price levels (2014, %)

Notes:

GDP per capita in PPS. Comparative price levels of final consumption by private households including indirect taxes.

Source: The processing of the authors on the basis of

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tec00114&plugin=1

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&plugin=1&language=en&pcode=tec00120

Furthermore, Table no. 3 shows price convergence. The low price level convergence has been caused by the following factors:

Low Czech inflation;

Depreciation of the CZK/EUR exchange rate as of November 2013.

Particularly the second factor contributed to the departure of the Czech price level from the euro area price level – in 2008, the Czech price level amounted to 74.8% of the euro area average (17). Price convergence represents one particular area, where it is advisable to compare the price levels of acceding countries to those of their main trading partners, as opposed to the euro area level. Calculations suggest that the comparison of the Czech price level to the price levels of its three main trading partners would result in a 7 p.p. lower gap in 2013 (see Helisek, Mentlik, 2015).

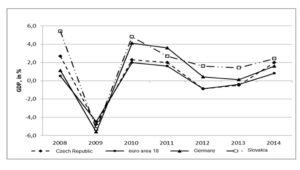

The correlation of the Czech business cycle to that of the euro area and the main trading partners can be expressed as the comparison of year-to-year changes in real GDP (Figure no. 1). The development of business cycles expresses about the same trend (namely the recession stage in 2009, recession or declining growth in 2012-2013).

Figure 1: Changes in real GDP (year-to-year comparison, %)

Source:http://ec.europa.eu/eurostat/tgm/table.dotab=table&init=1&language=en&pcode=tec00115&plugin=1

The processing of the authors

Overall, the real convergence criteria mainly show positive results as well.

Perspectives of the Euro Introduction

Many institutional measures have been taken in the Czech Republic in the course of the preparation for the euro adoption. These measures were also officially acknowledged by the European Commission in July 2007.

Institutional Preparation

The main measures in the form of strategic decisions and institutional measures are as follows:

- Euro Area Accession Strategy and Updated Euro Area Accession Strategy (2003, 2007);

- Institutional Arrangements for Introduction of the Euro (2005), which contain the establishment of the National Coordination Group for euro changeover in the Czech Republic (NCG) and of the national coordinator; in the period of 2007 – 2014, the NCG submitted nine reports on its activities to the Government;

- Choice of Scenario for the Introduction of the Euro (2006)– in the form of big-bang – i.e. one-step introduction of the euro for cash and noncash transaction (big-bang);

- National Euro Changeover Plan for the Czech Republic (2007); in the period of 2008 – 2010, the NCG prepared three Reports on the National Plan Fulfilment;

- In February 2008, a website of the Ministry of Finance dedicated to the euro introduction was launched – Euro Introduction in the Czech Republic (www.zavedenieura.cz);

- The Ministry of Finance prepared a draft General Act on the Introduction of the Euro in the Czech Republic (2008);

- Act on the Czech National Bank (CNB) that governs activities of the CNB following the euro introduction in the Czech Republic; it was vetoed by President Klaus on 3 June 2010;

- The Ministry of Finance and the Czech National Bank publish their annual Assessment of the Fulfilment of the Maastricht Convergence Criteria and the Degree of Economic Alignment of the Czech Republic with the Euro Area (since 2004);

- Each year (since 2004), the Government approves the Convergence Program of the Czech Republic, which is prepared by the Ministry of Finance and which mainly assesses the situation of public finance;

- In the period of 2007 – 2009, the NCG prepared six methodology texts (rules for conversion and rounding of monetary amounts, procedures for dual assessment, financial sector preparation, price development monitoring following the euro introduction, estimate of budgetary expenditure, and communication strategy) as well as the material Preparing the legal environment (March 2009).

As of April 2011, the period of the so-called reduced preparations starts, with further preparations only consisting in, for example, the monitoring of foreign experience, informing the public through dedicated websites, revision of methodology papers, etc.

Current Perspectives of the Euro in the Czech Republic

The discontinued preparations for the euro introduction and the negative position of Czech Governments, coupled with the negative position of the central bank, have also been reflected in the views of the Czech public. The development of public opinion (= voters) is shown in Figure no. 2.

Figure2: Development of public opinion concerning the euro introduction in the Czech Republic (%, 2001-2015)

Source: The processing of the authors on the basis of Czech Public Opinion Research Center, 2015, p. 2. Last survey of April 2015, 1011 respondents

It is clear from Figure no. 2 that the negative position on the euro started to prevail at the turning of 2006 and 2007:

- In April 2006, there were 45% of euro advocates compared to 43% of euro opponents;

- In April 2007, the results were 45% to 48%.

Therefore, the given change cannot be attributed to the financial crisis or the subsequent economic recession that started in the United States, later shifting to Europe, as the subprime mortgage crisis in the United States broke out during the summer of 2007; the banking crisis then broke out in the fall of 2008 (bankruptcy of Lehman Brothers on 15 September 2008). Some banks in Great Britain, German, Benelux, and Iceland started to experience problems at the time. However, the first year of recession in the EU was 2009.

Changing views regarding the euro are significantly associated with political changes in the Czech Republic:

- In November 2005, the Cabinet of the Czech Social Democratic Party decided to introduce the euro as of 1 January 2010;

- Right-wing Cabinet took office in September 2006, revoking the euro introduction date one month later.

Therefore, the development of public opinion (= views of voters) is related with the negative position of the new political representation – not only to the euro introduction, but to the European integration as a whole The negative public opinion subsequently affected the decisions on further preparations for the euro introduction – these preparations were reduced. The lack of interest in the euro at the time was caused by the previous lack of interest in the euro. It is a phenomenon that is observed in the economics, e.g. with regard to the labour market development, described as the labour market hysteresis (current unemployment is caused by previous unemployment). With regard to monetary integration, the euro adoption hysteresis can be observed

It is also clear from Figure no. 2 that the views of the public regarding the euro introduction have changed since 2014. This has also been affected by political positions. A positive position on the euro introduction was expressed in the Policy Statement of the new coalition Government of the Czech Republic (January 2014): “The Government shall actively strive to create conditions conducive to the adoption of the euro.” “The Government shall support steps towards the deeper coordination of economic and fiscal policy and towards the restoration of confidence in the European financial sector. It shall revise the existing reticent opinions on monetary integration and financial cooperation.” (highlighted by M. H.) According to the Prime Minister, the euro could be adopted in 2020[1] or in 2019-2021according to the Minister of Industry and Trade.[2]

Fear of inflation

As described in the book 10 years of euro:success? by Lacina, Rozmahel and Rusek, research results that rely on Eurobarometer surveys suggest that the price expressed in the original national currency is a benchmark for more than 50% of respondents in the newly acceding countries, for the minimum period of one year. For daily consumer goods this figure goes up to more than 70% of respondents[3]. Experiences with the fears of price increases caused that the fight against this phenomenon has become one of the key areas of practical preparations for the accession into the euro area in new EU Member States.

Legal requirements:

- usage of dual display of prices and other selected monetary amounts,

- frequent commercial inspections monitor the compliance with conversion rules,

- statistical offices perform more frequent price monitoring for sensitive market basket items,

- chambers of commerce promote fair prices code of conduct,

- consumer associations publish blacklists of merchants that carried out unsubstantiated price increases.

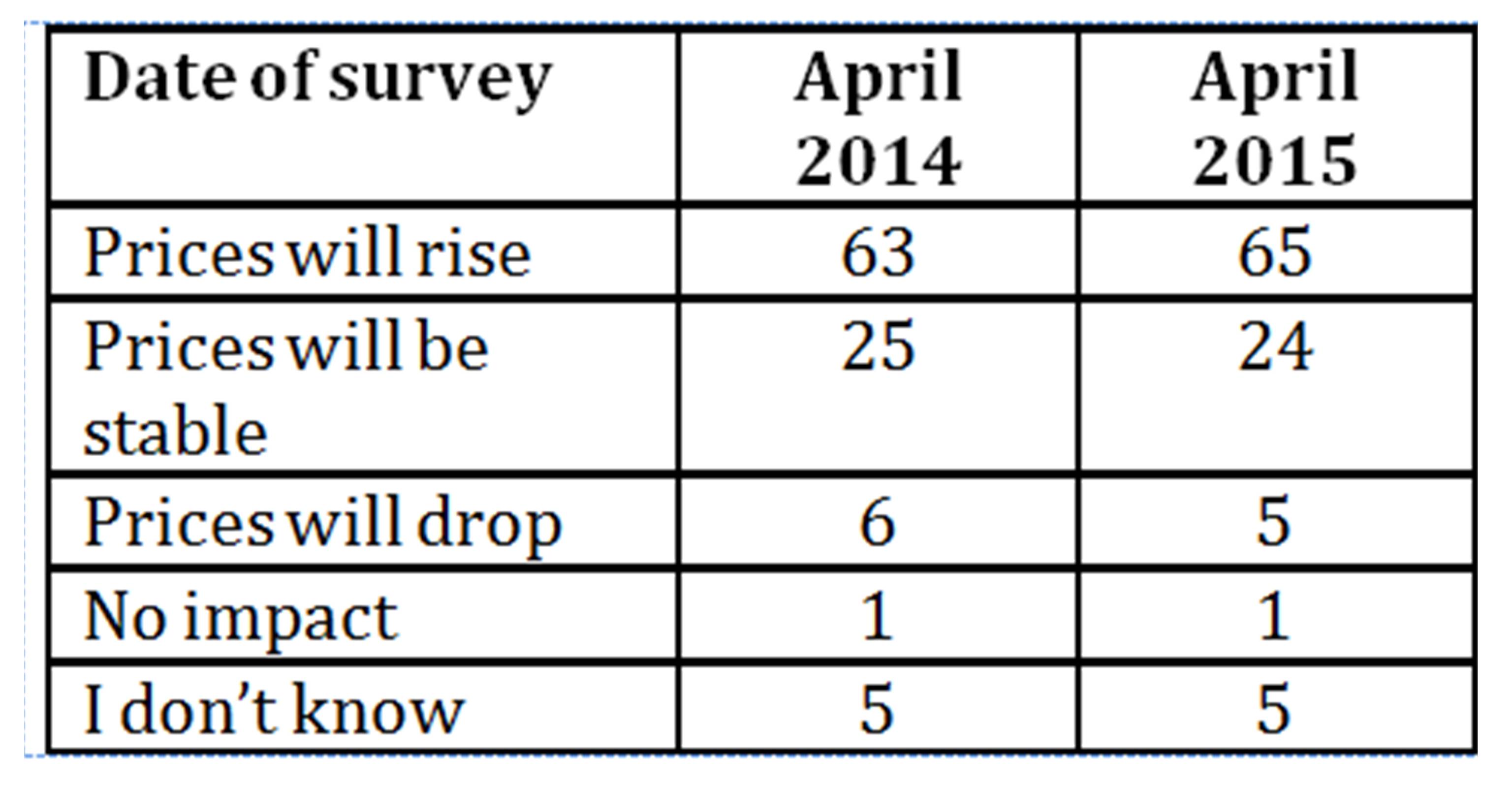

In a Eurobarometer survey of April 2015 conducted in seven Member States that have yet to adopt the euro (Bulgaria, Czech Republic, Hungary, Poland, Romania, Croatia, and Sweden), 7022 respondents were given the following questions: What impact, if any, will the euro introduction have on the price level? The structure of their answers is graphically shown in Table no. 4.

Table 4: Impact of the euro introduction on the price level (amount of respondents, %)

Source: The processing of the authors on the basis of European Commission. 2015 Flash Eurobarometer 418

In the case of the Czech Republic, 73% of respondents are convinced that the euro introduction will result in price increase, 19% of respondents believe the prices will remain stable, 3% of respondents think the prices will be reduced, and 4% of respondents believe the euro introduction would not have any effect on prices[1].

Specialized materials show that there are no objective reasons for prices to increase following the euro introduction; however, the aforementioned results indicate that people still expect price increases. Let us mention several examples that rather support such expectations. Data from countries that have already introduced the euro show that a cup of coffee, restaurant prices, parking fees, and text message prices are more expensive than before the euro changeover.

Let us provide several examples that show certain rationale behind such concerns. For example, if we assume a conversion rate of 24 to 25 CZK per 1 EUR, it will be very complicated to convert the value of points that are used to measure the performance of doctors. General practitioners currently receive CZK 1.07 per point, non-resident specialists receive CZK 1.05, and emergency services receive CZK 1.03. Following the euro conversion, they would all get EUR 0.04 as a result of the conversion and subsequent rounding. Another example includes prices of mobile phone operators or text message prices, as appropriate. At present, one text message costs about CZK 1 – i.e. hundred messages cost CZK 100. Upon conversion using a conversion rate of CZK 27.20 / EUR, one text message would cost EUR 0.0367, i.e. EUR 0.04 after rounding off. Hundred messages would cost EUR 4, i.e. CZK 108.80. In other words, the same service would be CZK 8.80 more expensive – i.e. price increase of 8.8%[2].

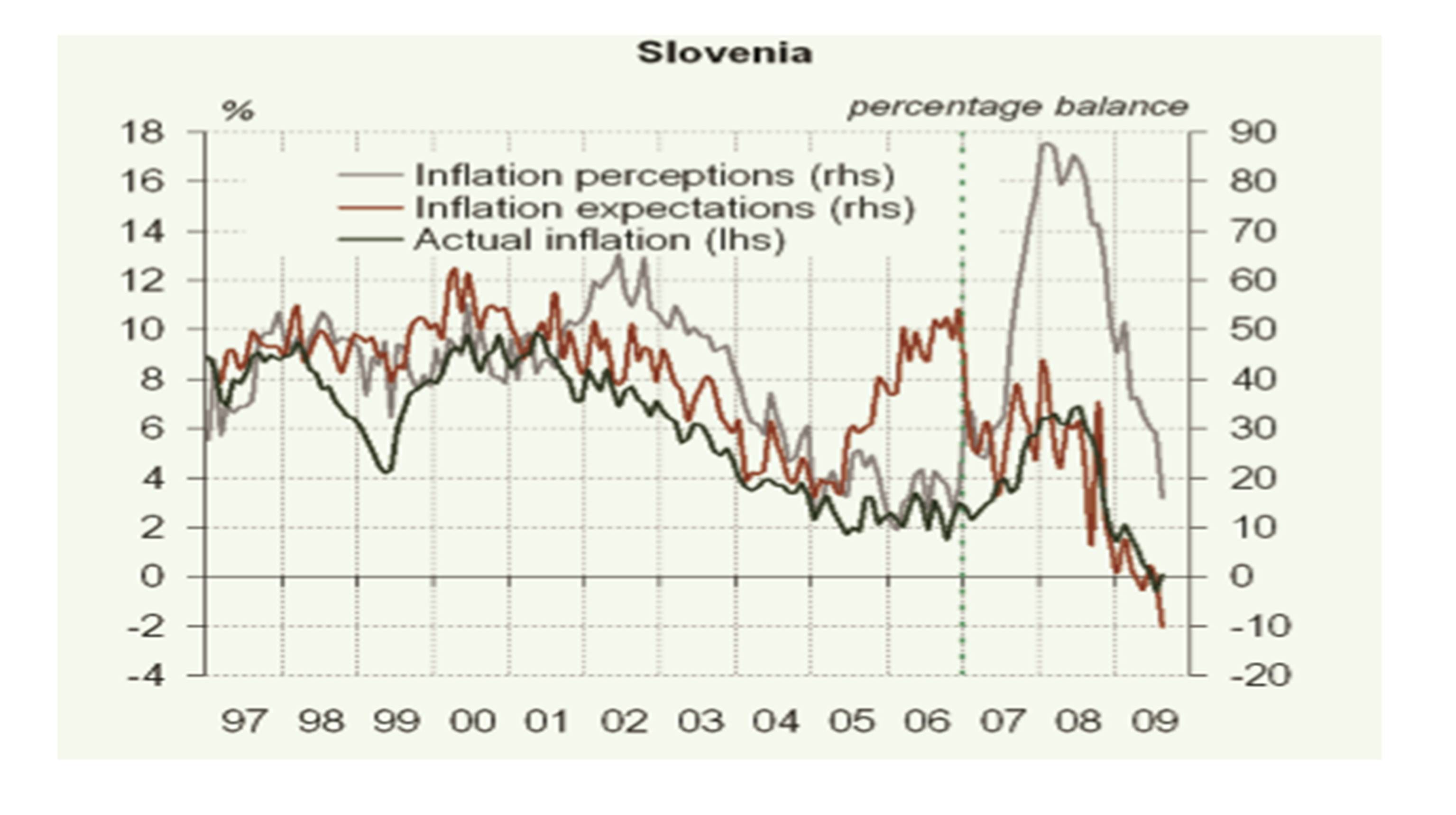

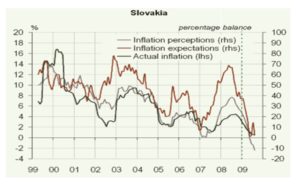

The fears of inflation due to euro introduction, which are stated by the aforementioned Eurobarometer survey, are not surprising. These fears have also been present in new Member States, which already have euro already adopted. Specifically, in Slovakia, the actual inflation right before the euro introduction was almost 3%, however inflation expectations were much higher. In Slovenia, there were even larger concerns. Data about the actual and expected inflation are in Figures no. 1 and no. 2 in the attachment.

Actual and perceived inflation

The essence of perceived inflation is, that even though an actual (officially measured) inflation does not show any extraordinary increases during the euro introduction period, the public is generally convinced that the euro changeover resulted in higher inflation.

However, some subsequent research studies that focused on explaining the aforementioned phenomenon brought many interesting findings:

- The inflation increase resulting from the rounding off of converted amounts/prices was estimated at about 0.3 p.p.[3]

- The significant variation between the actual inflation and the perceived inflation was promoted by the psychology of consumers’ perception of price changes that is more sensitive to price increases than to declining prices, tends to apply partial adverse experiences to the overall development of prices, and is unable to weigh the overall increase for individual items by their share in the total expenditure.

- Any inflation pressures were blamed on the euro, although many of them (tax adjustments, weaker euro exchange rate, rising energy prices, etc.) were not immediately related to the euro introduction.

Perceived inflation falls within the category of psychological quantities that have their own measurement processes. The European Commission organizes and finances systematic public opinion surveys targeting the aforementioned area, entitled Business and Consumer Surveys. These surveys take place on a monthly basis, in the form of telephone inquiry. The questionnaire includes six questions that examine how respondents perceive price increases (expectations).[4]

The result of the measurements of perceived inflation is so called balance statistics, which shows consumers’ opinions, using an index in the range from-100to +100:

if the value is +100, all believe that prices increased significantly,

if the value is -100, all believe that prices decreased.

[1]European Commission.2015 Flash Eurobarometer 418.

[2]Similar approach is also taken by Jan Stuchlik, for example – http://www.penize.cz/inflace/43252-proc-euro-udajne-zpusobuje-drahotu

[3] European Central Bank. 2007, p. 68

[4] See for example Dedek, O. 2014, p. 121.

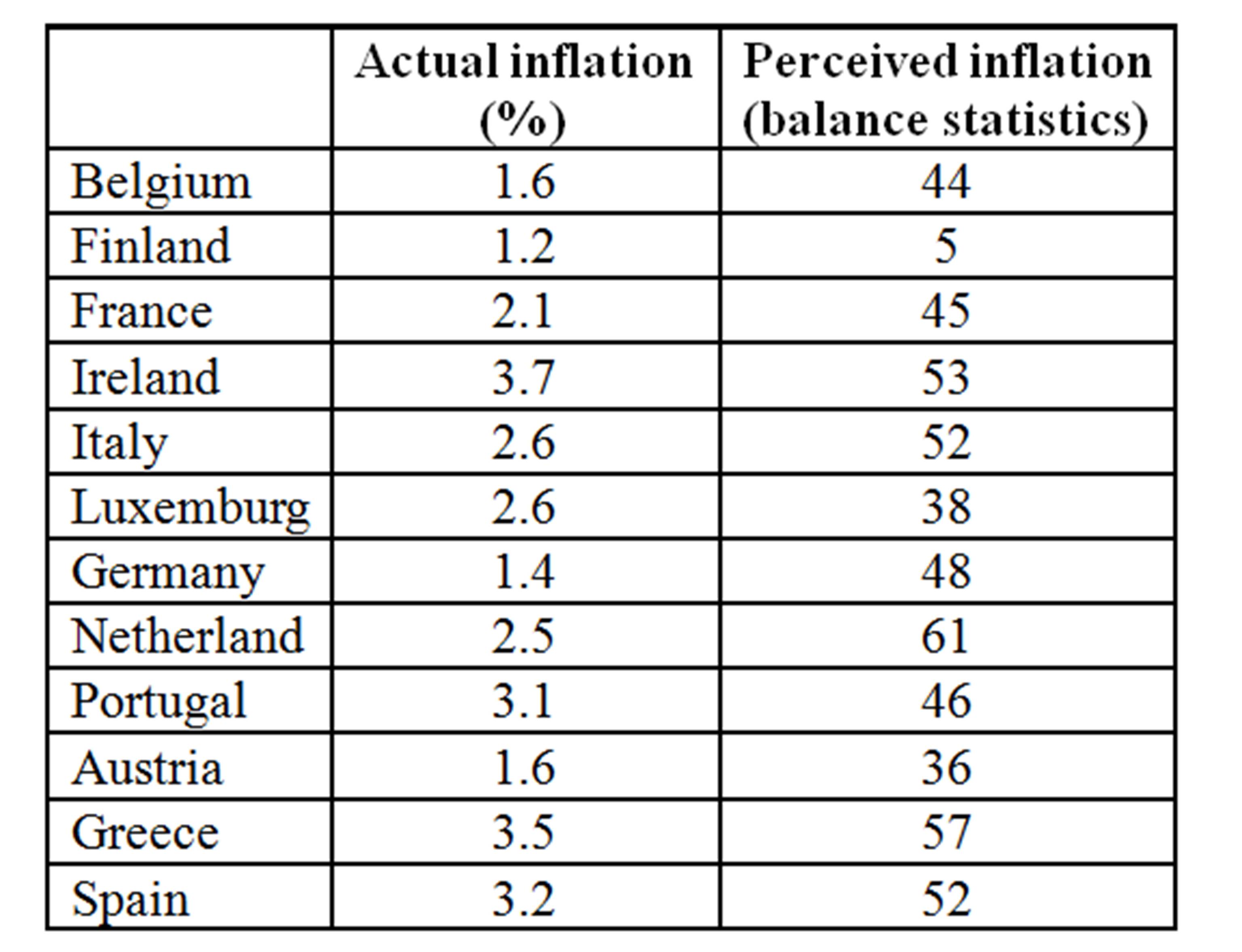

Table 5: Actual and perceived inflation in euro area countries

(2002-2004, average annual data)

Source: The processing of the authors on the basis of European Central Bank. 2007, p. 64.

Tableno.5 shows that the actual inflation after the introduction of euro for cash payments fluctuated around 2%. Irrespectively of the aforementioned fact, consumers came to a conclusion that the euro introduction resulted not only in a price jump, but also in a permanently higher inflation. As shown in Table no. 4, this feeling was dominant in all euro area countries with the exception of Finland. On average, in 12-euro area countries reached in late 2002 the index of balance statistics63[1], which means the prevailing views on the impact of the euro introduction on the inflation increasing.

The difference between actual and perceived inflation (perceived inflation being higher than actual) was observed also in other new EU member countries. This difference was observed both in the case where the actual inflation rose (Slovenia), and in the case where the actual inflation fell (Slovakia) – see Figures in the Attachment.

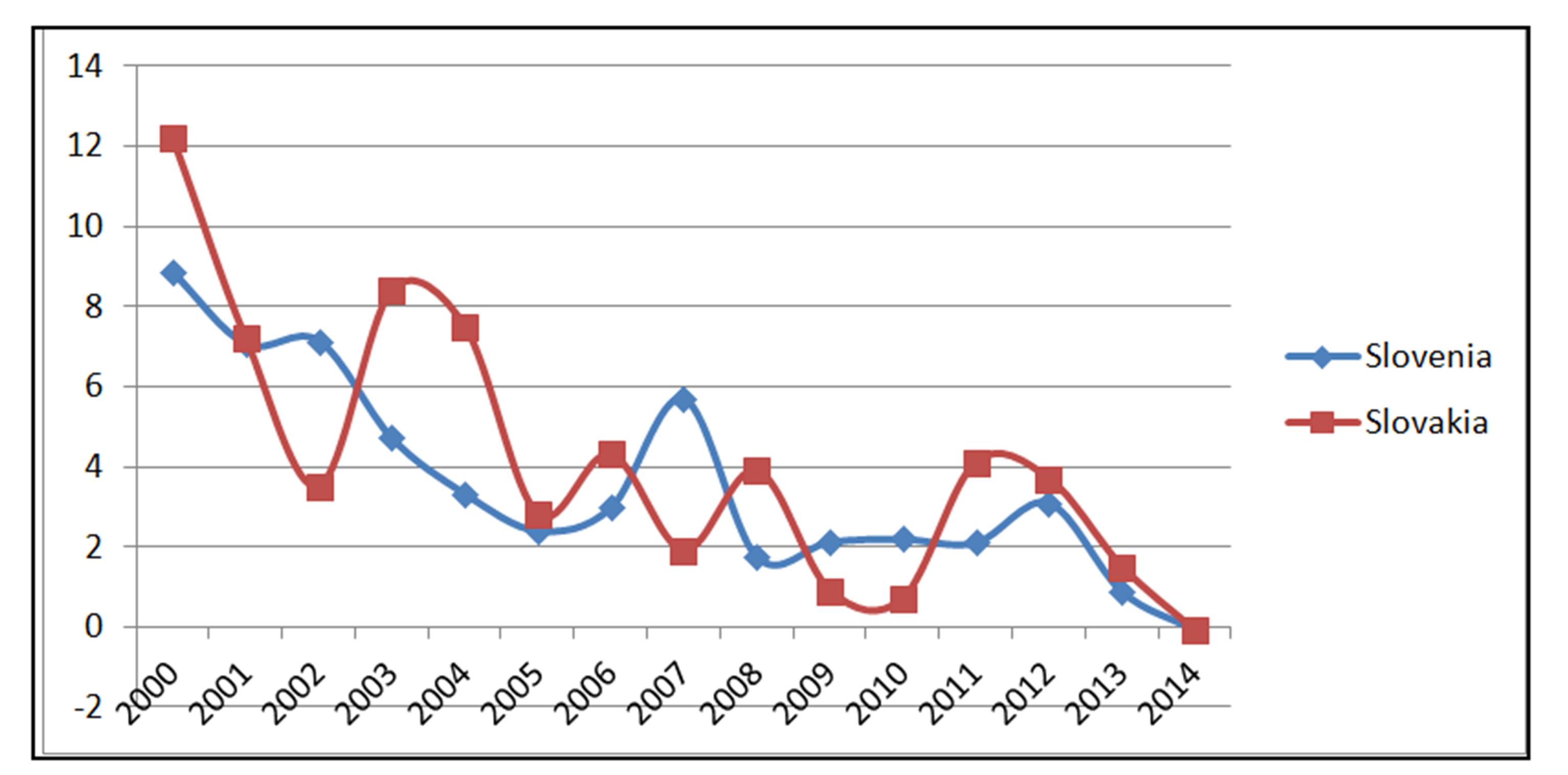

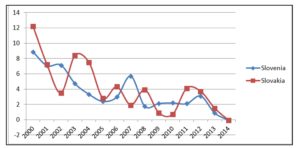

Experiences in Slovakia and Slovenia with the inflationary impacts of the euro introduction

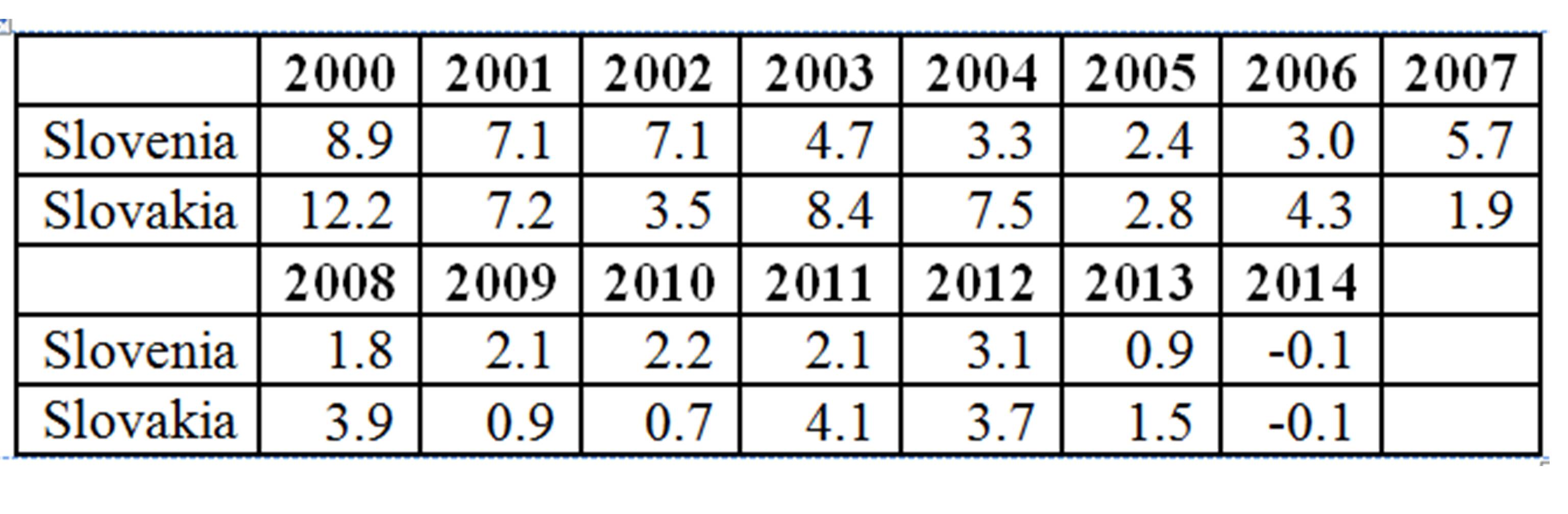

The euro introduction process in Slovakia and Slovenia confirmed that, similarly as in other countries adopting the euro, also here people were concerned about increase prices as a result of the euro changeover. In this regard, many parallels can be expected for the euro adoption in the Czech Republic. In spite of these negative expectations, they were largely successfully eliminated, and actual inflation didn’t reach high levels, that were expected. That is illustrated in Table no. 6 and Figure no.4.

Table 6: Development of inflation in Slovenia and Slovakia (2000 – 2014)

[1] European Central Bank. 2007, p. 64.

Source: The processing of the authors on the basis of http://www.nbs.sk/_img/Documents/_Publikacie/OstatnePublik/ukazovatele.pdf

http://www.inflation.eu/inflation-rates/slovenia/historic-inflation/cpi-inflation-slovenia.aspx

Figure3: Development of inflation in Slovenia and Slovakia (2000 – 2014)

Source: The processing of the authors on the basis of http://www.nbs.sk/_img/Documents/_Publikacie/OstatnePublik/ukazovatele.pdf

http://www.inflation.eu/inflation-rates/slovenia/historic-inflation/cpi-inflation-slovenia.aspx

The actual inflation after the euro introduction in Slovakia (early 2009) was around 3%, however, expected inflation was higher. According to the official calculations of the National Bank of Slovakia, the impact of the euro changeover on inflation was ultimately lower than estimated – i.e. 0.12 to 0.19 p.p.[1] These results were achieved by applying a set of several measures (mentioned in section 6), targeting the protection of consumers from any abuse of the transition to the new currency by merchants and businesses, which would have impact on the increasing of actual inflation. Of course, one of the factors that contributed to lowering the inflation (0.9% for 2009) was the economic recession in this year.

Another problem was to limit the perceived inflation from rising, and therefore limiting the negative stance of citizens towards the new currency. This was achieved in Slovakia by organizing an information campaign targeted at the general public, with special emphasis on the phenomenon of perceived inflation. Price surveys of selected consumer prices proved to be one of very effective instruments, with the objectivity and professionalism of such surveys ensured by the statistical office. These statistical surveys took place in regional cities several days after the euro introduction. Quick publication of results eliminated various speculations and assumptions, while also preventing any speculations on the part of the media.

Also in Slovenia, there were concerns about increasing prices following the euro changeover. In reality, inflation went down in January 2007 (following the euro introduction) compared to December 2006, as a result of end of season sales. The annual inflation decline from 3% to 2.8% in January was mainly caused by lower energy prices. Overall, the prices increased by 1.3% during the first months of 2007, compared to 1.5% in the same period of 2006.Throughout 2007, the inflation has been relatively high at 5.7%. This growth was caused by the inflation in the second half of the year going up due to the financial crisis. An independent study by the Slovenian Institute of Macroeconomic Analysis and Development expected the impact of the euro introduction on inflation at 0.24 p.p.[2]Similarly Eurostat quantified the impact of the euro introduction on consumer prices at 0.3p.p.[3]

Overall, the experience in old and new member states of the euro area does not indicate inflationary impact of the introduction of the euro. In addition to these experiences existing development of inflation in the euro area must be taken into account as another factor that affects the inflation after the introduction of the euro (Table no. 7).

Table 7: HICP – inflation rate Annual average rate of change (%), EA 19

Source: The processing of the authors on the basis of

http://ec.europa.eu/eurostat/tgm/table.do?tab=table&init=1&language=en&pcode=tec00118&plugin=1

Inflation in the euro area is very low. In many countries was even mild deflation (Greece, Spain, Cyprus, Portugal, Slovakia, Finland) in the years 2014 and 2015. The European Central Bank fears of extension of deflation into other countries. In these circumstances, we can´t expect that the introduction of the euro causes the increasing of inflation.

Conclusion

Discussions relating to the euro introduction in the Czech Republic are topical. The following circumstances corroborate early introduction of the euro:

- Most institutional preparations for the euro introduction have already been carried out;

- Czech economy complies with the Maastricht convergence criteria (required nominal convergence);

- The real convergence level to the euro area economy is sufficient as well;

- There has been a positive change in the position of the significant part of the political representation in terms of the euro introduction with subsequent more positive views of the public on the euro.

The Czech Republic, as another country adopting the euro in subsequent stages, can capitalize on the knowledge and experience with prior introduction of currencies in other countries. Traditionally, the Czech Republic has been known as a euro-sceptic country, with the euro lacking strong support of the general public. Therefore, a thoroughly prepared information and communication campaign will be absolutely crucial for the euro changeover process.

The Czech Republic can use the experiences of the euro introduction in Slovenia and Slovakia, where despite expectations of high inflation (fears of inflation), it was possible to maintain the inflation at a low level. At the same time, the Czech Republic has to expect higher perceived inflation, in comparison to the actual inflation, and pay attention to it in its communication and information campaign.

Acknowledgement

The paper has been prepared within the project Accession of the Czech Republic to the euro area – preparations, procedures, and expected impact, supported by the Specific University Research Funds at the University of Finance and Administration.

(adsbygoogle = window.adsbygoogle || []).push({});

References

- ‘The Czech Republic’s Updated Euro-area Accession Strategy (Joint Document of the Czech Government and the Czech National Bank)’ (2007), [Online],[Retrieved October 20, 2013], http://www.zavedenieura.cz/en/documents/euro-area-accession-strategy

- Centrum pro vyzkum verejneho mineni (Center for Public Opinion Research). (2015), ‘Obcane o prijeti eura a dopadech vstupu CR do EU – duben 2015,(Citizens on the euro adoption and the impacts of Czech accession to the EU – April 2015). [Online], [Retrieved May 20, 2015],http://cvvm.soc.cas.cz/media/com_form2content/documents/c1/a7382/f3/pm150512.pdf

- Czech National Bank. (2014), ‘Analyses of the Czech Republic´s Current Economic Alignment with the Euro Area,’ [Online], [Retrieved May 20, 2015],http://www.cnb.cz/miranda2/export/sites/www.cnb.cz/en/monetary_policy/strategic_documents/download/analyses_of_alignment_2014.pdf

- Dedek, O. (2014), Doba eura. Uspechy i nezdary spolecne evropske meny, Linde, Praha. (The era of the euro. Successes and failures of the common European currency.)

- European Central Bank. (2007), ‘Monthly Bulletin, May 2007’ [Online], [Retrieved May 20, 2015],https://www.ecb.europa.eu/pub/pdf/mobu/mb200705en.pdf

- European Central Bank. (2014), ‘Convergence Report June 2014,’ [Online], [Retrieved May 20, 2015], http://www.ecb.europa.eu/pub/pdf/conrep/cr201406en.pdf?4394e06aee28a2d26873f0fde5d0cf96

- European Commission. (2014), ‘Convergence Report 2014,’ [Online], [Retrieved May 20, 2015], http://ec.europa.eu/economy_finance/publications/european_economy/2014/pdf/ee4_en.pdf

- European Commission.(2007), ‘Eurobarometer 68.Narodni zprava. Ceska republika. Podzim 2007,’ (National Report. Czech Republic. Fall 2007). [Online], [Retrieved May 20, 2015],http://ec.europa.eu/public_opinion/archives/eb/eb68/eb68_cz_nat.pdf

- European Commission. (2015), ‘Flash Eurobarometer 418. Introduction of the euro in the Member States that have not yet adopted the common currency,’ [Online], [Retrieved May 20, 2015]. http://ec.europa.eu/public_opinion/flash/fl_418_en.pdf

- Helisek, M. (2015) ‘Political Economy of the Euro Introduction in the Czech Republic,’ In: Pavlat, V. – Schlosssberger, O. (ed.) Proceedings of the 7th International Conference on “Financial Markets within the Globalization of World Economy”, VŠFS EUPRESS, Prague pp. 82-93.

- Helisek, M. et al. (2009), Euro v Ceske republice z pohledu ekonomu, Ales Cenek, Plzen. (The euro in the Czech Republic from the perspective of economists).

- Helisek, M. and Mentlik, R. (2015), ‘Price Convergence to the Euro Area and Preparedness of the Czech Republic for the Adoption of the Euro,’International Journal of Business and Management Study. 2 (1), 155-159.

- Helisek, M., Mentlik, R. (2013) ‘The Debt Crisis in the Euro Area and Change the Operating Conditions of Monetary Union,’ In: Economic Policy in the European Union Member Countries. Conference Proceedings, VSB – Technical University of Ostrava, Ostrava, pp. 116-122.

- Janackova, S. (2014), Peripetie ceske ekonomiky a meny aneb nedejme si vnutit euro. InstitutVaclava Klause, Praha. (Peripety of the Czech economy and currency, or, let’s not have the euro forced on us).

- Jemec, N. (2010) ‘Inflation Perceptions and Expectations around Euro Change Over. Banka Slovenije’, Prikazi in analize 1/2010. [Online], [Retrieved October 20, 2013],https://www.bsi.si/library/includes/datoteka.asp?DatotekaId=3853

- Lacina, L. et al. (2008), Studie vlivu zavedeni eura na ekonomiku Ceske republiky. 2nd revised edition incl. suggestions from a peer-review process, Martin Striz, Bucovice. (Study of the impact of the euro adoption on the economy of the Czech Republic)

- Lacina, L., Rozmahel, P. and Rusek, A. (2009), 10 years of euro: success?, Ales Cenek, Plzen.

- Mach, P. (2012), Jak vystoupit z EU. 2nd revised edition. Dokoran, Praha. (How to leave the EU)

- Ministry of Finance of the Czech Republic and the Czech National Bank.(2014), ‘Assessment of the Fulfilment of the Maastricht Convergence Criteria and the Degree of Economic Alignment of the Czech Republic with the Euro Area,’ [Online], [Retrieved May 20,2015], http://www.zavedenieura.cz/en/documents/fulfilment-of-maastricht-criteria

- Ministry of Finance. Czech Republic.(2015), ‘Convergence Programme of the Czech Republic April 2015,’ [Online], [Retrieved May 20, 2015], http://www.zavedenieura.cz/en/documents/convergence-programmes

- National Bank of Slovakia. (2009), ‘Impact of the euro introduction on inflation in the Slovak Republic in January 2009,’ [Online], [Retrieved May 20, 2015]. http://www.nbs.sk/_img/Documents/PUBLIK/MU/vplyvEURA.pdf

22.National Coordination Group for Euro Changeover in the Czech Republic.(2007),‘National Euro Changeover Plan for the Czech Republic,’[Online], [Retrieved May 20, 2015], http://www.zavedenieura.cz/en/documents/national-euro-changeover-plan

Appendix

Development of perceived, actual and expected inflation in Slovenia and Slovakia

Figure 1: Inflation in Slovenia

Figure 2: Inflation in Slovakia

Source: Jemec, N. (2010), pp. 17, 18. Reprinted with permission of the author.

Notes

Arguments against this view see in the paper from Helísek, Mentlik (2013, p. 121): “Countries acceding to the European Union enter an integration group that currently has its specific institutional form. However, when acceding to the EU, it is necessary to take into account the fact that the continuing integration processes will lead to institutional changes. The accession to the EU may not be conditioned by the assumption that the integration processes will come to a standstill.”

Precise data taken from: Ministry of Finance of the Czech Republic and the Czech National Bank. 2014, p. 3.

The Czech Republic’s Updated Euro-area Accession Strategy, p. 1.

ECB : European Central Bank, 2014, p. 137.

The Czech Republic was identified as a good example of timely preparation even without a set target date. Commission of the EC, Fifth Report, 2007, p. 10.

For more details see, for example, Helisek et al., 2009, pp. 24-27

This view is also supported in the commentary to the Eurobarometer survey conducted in the fall of 2007: “However, the public opinion regarding this European project [i.e. the euro] were evidently impacted by the views of the predominant part of the Czech Government coalition: the support went down by 7 percentage points, currently being significantly lower than the long-term stable average of EU 27.” (European Commission, 2007, p. 27).

European Commission.2015 Flash Eurobarometer 418.

See Helisek, M., 2015, pp. 89-90.

http://www.vlada.cz/cz/media-centrum/dulezite-dokumenty/programove-prohlaseni-vlady-cr-115911/

[1]http://www.denik.cz/ekonomika/euro-v-cesku-premier-mluvi-o-roku-2020-2014041