Introduction

In late 2019, an unfamiliar virus emerged in the Chinese city of Wuhan, home to over 11 million individuals. The illness, which featured flu-like symptoms but more serious complications, rapidly developed into an epidemic. Its indications comprised high fever, exhaustion, dry cough, muscle pain, and respiratory issues. Despite attempts to contain it, the virus eventually spread beyond China, with early 2020 seeing its appearance in other nations. It is believed that the virus propagated most

significantly in regions with robust migration networks (Kincses, 2020). The World Health Organization (hereinafter WHO) declared an outbreak of COVID-19 a public health emergency of international concern in January 2020 and a global pandemic in March 2020 (Zhang and Lange, 2021). COVID-19 is a viral respiratory disease caused by a fatal infection (SARS-CoV-2) which brought about the 2019 global pandemic (Aqeel et al., 2021).

The year 2022 saw the outbreak of a new crisis – the War of 2022. Amidst the turmoil and devastation, nations struggled to combat the virus that had first surfaced in 2019. “Governments have attempted to cooperate in order to prevent transmission, which has involved multi-directional collaboration that takes into account both economic and social consequences.” Despite these efforts, the level of epidemiological measures and their implementation varied significantly from state to state, depending on each country’s decisions. In nearly all instances, closures were implemented to prevent the development of a more severe health crisis, even if it meant a downturn for the economy. Countries leading the global response have had to weigh the trade-offs between slowing the spread of the epidemic and safeguarding the economy (Chen, 2020). Collaborative efforts were also necessary between countries to jointly fund research programs that could bring us closer to cures and vaccines. It is estimated that the epidemic’s impact and the crisis it caused will amount to approximately €1,500 billion (Balázs, 2020).

Aside from its detrimental effects on the health system, the pandemic has hit the tourism industry the hardest, with government-mandated measures serving as the primary cause. The War of 2022 exacerbated the damage, making recovery more challenging. “Industries such as automotive, extractive, clothing, and textiles have also faced limitations” (Nicola et al., 2020), primarily due to the breakdown of supply chains and the sudden decline in global demand. In many cases, travel restrictions have prevented people from visiting destinations, but concerns have also contributed to the industry’s downturn (Ahmad, 2020). There is a significant correlation between reduced mobility and a decline in industrial production. In other words, the more stringent public health measures, the more significant the drop in industrial production (Czeczeli, 2020). However, the digital advertising market (webshops, webinars), courier companies, pharmaceuticals, chemicals, and personal protective equipment (masks, gloves, protective gear) have seen a clear positive impact (Fernandes, 2020). It is also expected to have a favorable effect on the adoption and use of teleworking and, subject to certain constraints, on financial services. The former could also have a positive impact on reducing environmental damage caused by vehicle usage. Companies producing pharmaceuticals, vitamins, and other nutritional supplements could benefit and strengthen further in the context of vaccines.

The onset of the virus was nearly simultaneous across central European countries, with the first case appearing in the Czech Republic on March 1, 2020, followed by Hungary and Poland on March 4, and Slovakia on March 6. By the end of May, Poland had recorded 19,268 cases, the Czech Republic had 8,647, Hungary had 3,598, and Slovakia had 1,295 cases (according to corona.gov statistics pages). Within three weeks of the initial cases, the V4 countries implemented restrictions and declared states of emergency. Prior to the initial outbreaks, some preventative measures were already in place, such as the suspension of visas for Chinese citizens in the Czech Republic and the introduction of random border controls in Slovakia. The countries minimized public life, closing schools, restaurants, cafes, pubs, shopping centers, and banning mass events. A mandatory quarantine was enforced for those returning from abroad, and masks or scarves covering the nose and mouth were made compulsory. Although the number of cases decreased during the summer of 2020, the second wave of infections began to surge as restrictions were lifted and the virus spread more rapidly.

The impact of the War of 2022 added to the difficulties faced by these countries. Ukraine, a neighboring country, was directly involved in the conflict, and this had an impact on the response to the pandemic. In addition, the conflict disrupted supply chains and transport routes, making it harder to get essential medical supplies and equipment to where they were needed. This further exacerbated the already challenging situation faced by central European countries in their fight against the pandemic.

As the COVID-19 outbreak emerged in central Europe, countries like the Visegrad Four (V4) were quick to respond and implement measures to flatten the epidemic curve and reduce the number of daily cases. This was particularly important in the context of ongoing conflict in neighboring Ukraine, where a weakened healthcare system would struggle to cope with a surge in COVID-19 cases. The use of masks and reducing the number of contacts were common practices in all four countries, with mandatory mask-wearing becoming the norm during the second wave. The V4 countries were particularly effective in taking action quickly to prevent the spread of the virus, setting an example for other countries to follow (Sevcik, 2020). However, it is important to note that the war in Ukraine has also played a role in the pandemic response of the V4 countries. The conflict has created additional challenges in terms of border control and cross-border travel, which has affected the ability of the countries to implement consistent measures. Moreover, the war has led to a high number of internally displaced persons and refugees, who are particularly vulnerable to the virus.

The economic implications of the pandemic are still uncertain. It is widely acknowledged that the outbreak is contributing to a global crisis. Emerging economies, which are highly exposed to global developments, are likely to be the most vulnerable and will need to enhance their business resilience and leverage IT technologies (Bajzíková et al., 2017).

The Visegrad Four countries are no exception to the economic impact of the pandemic. All four countries have export-import ratios above 100%, indicating that the road to recovery will be challenging for them. The ongoing conflict in Ukraine, which has affected the region’s stability and economic growth, is also adding to the challenge.

Aims and Methodology

The aim of this work is to examine the firms with the highest sales in the V4 countries in terms of asset turnover ratio during the Covid-19 pandemic, including the recent 2022 war. Additional goals include introducing the pandemic and war situation and its relationship with the V4, identifying the companies with the largest sales in the four countries, and calculating the asset turnover ratio of these firms for 2018-2022. This study aims to analyze how the V4’s biggest companies have responded to the health crisis, taking into account the recent impact of the war. To conduct the analysis, we utilized the HitHorizons database, which creates a user-friendly data platform to present public company data in a comprehensive format. We selected companies with the highest sales in each country, including:

- AUDI HUNGARIA

- Polski Koncern Naftowy Orlen

- Škoda Auto

- Volkswagen Slovakia

The asset turnover ratio was calculated based on the companies’ publicly available annual reports, using the following formula: Assets turnover ratio= Sales/Assets. The ratio shows the number of times total assets are turned over in a year, indicating how much sales a firm can generate with the resources available.

Results

The year 2020 was marked not only by the COVID-19 pandemic, but also by the outbreak of a war in 2022. The first COVID-19 patient in Europe was diagnosed on January 24, 2020 (Lescure, 2020), and governments around the world implemented diverse and adapted interventions to mitigate the negative economic effects. Measures included direct intervention to protect jobs, such as paying part of wages, and in the V4 countries, the state took over 40-60% or even 80% of the wage burden on businesses to support job retention (Tamásné, 2020). Other interventions included reductions in administration, sick pay during quarantine, low-interest loans and non-repayable subsidies to support businesses, legal protection, and deferral and moratorium measures. The reduction of the burden on businesses could also be of a different nature, such as halving the business tax rate in the small and medium-sized enterprise sector in Hungary (Kovács 2020), or monetary measures like cuts in the base rate in the Czech Republic and Poland. Country-specific interventions were also implemented, such as the awarding of diplomas without language exams in Hungary, the payment of care allowances to stay-at-home parents in Slovakia, the increase of the share of domestic food to 50% in the Czech Republic, and the mass retraining of (former) employees in critical sectors. In this light, we now present the selected companies and calculate their asset turnover ratio.

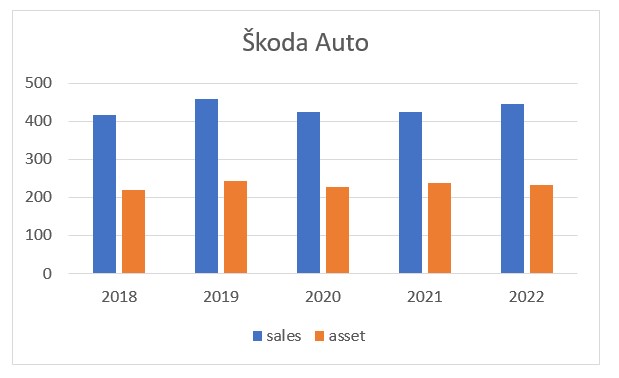

Fig 1. Sales and assets at Skoda Auto in 2018-2022 in CZK million

Source: Authors’ own work based on annual reports

Škoda Auto has a rich history dating back to 1895 when Václav Laurin and Václav Klement established the tradition of Czech car manufacturing. Over the years, the company has remained a prominent player in the automotive industry and has been a part of the VOLKSWAGEN Group for almost 30 years. Today, it has a strong global presence with ten model ranges and is recognized as a pillar of the Czech economy, providing employment to over 35,000 people in the Czech Republic. ŠKODA AUTO is committed to being a good neighbor in every region where it operates and has production plants in Mladá Boleslav, Kvasiny, and Vrchlabí. The covid crisis interrupted the growth dynamics of the company, but sales in 2020 did not fall below the 2018 level, and in 2022 they managed to return to growth – see Figure 1 (Škoda Auto, 2020).

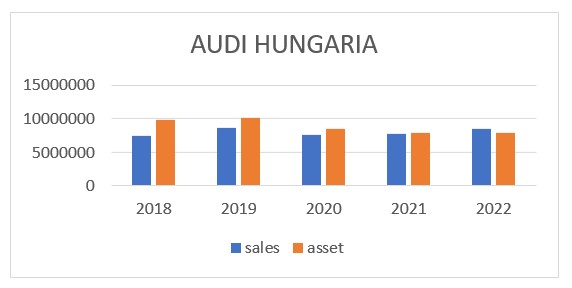

Fig 2. Sales and assets at AUDI HUNGARIA in 2018-2022 in HUF million

Source: Authors’own work based on annual reports

The company’s engine manufacturing activities started in August 1994 with the series’ production of four-cylinder engines, followed by the production of six- and eight-cylinder engines in 1997. Over the years, the engine production portfolio has steadily expanded. Today, more than 1.6 million units and nearly 140 engine types are produced in Győr. In 2018, a completely new era began in the life of the Company with the series’ production of electric engines, which have since been produced in an 8,500 m2 production hall and were first used in the new Audi e-tron. With the production of electric motors, AUDI HUNGARIA Plc. has entered a completely new and forward-looking field of competence. We can say from figure 3 that this company has been worse affected by the covid crisis (for the moment) than by the war in 2022, although we cannot take this as a fact, as the war is still going on. Their year 2022 was better than 2021 in terms of the indicators examined, but they are still not up to 2019 levels.

Fig 3. Sales and assets at Polski Koncern Naftowy Orlen in 2018-2022 in PLN million

Source: Authors’ own work based on annual reports

Orlen, also known as Polski Koncern Naftowy Orlen, is a state-owned oil refining and petrol retailing company based in Poland. The company is a prominent European listed corporation, operating extensively in Poland, the Czech Republic, Slovakia, Germany, the Baltic States, and Canada. Orlen was established through the merger of two state-owned petrochemical companies – Centrala Produktów Naftowych and Petrochemia Płock, responsible for petroleum retail and oil refineries in Poland, respectively. The merger took place in 1999, and the company was subsequently renamed Polski Koncern Naftowy (PKN) and later rebranded as Orlen. While the Polish government retains a 27% stake in the company, Orlen has grown into a significant player in the industry. Figure 3 shows that even pandemics and wars have not been able to prevent large-scale growth. (Orlen, 2022).

Fig 4. Sales and assets at Volkswagen Slovakia in 2018-2020 in EUR million

Source: Authors’ own work based on annual reports

On 7 December 1998, Volkswagen Slovakia, a.s. was founded with a primary focus on manufacturing and assembling motor vehicles and components, including gearboxes, tools, equipment, and pressed components. The company operates three plants located in Bratislava, Stupava, and Martin, all situated in Slovakia. As of 31 December 2018, the sole owner of the company, with a 100% stake, was Volkswagen Finance Luxembourg S.A. As we can see in the Chart 4., Volkswagen Slovakia has the largest ratio difference between sales and assets, and this will be reflected in the asset turnover ratio. The company has also been negatively affected by the crisis in terms of sales, but they were even able to increase the number of assets (Volkswagen, 2020).

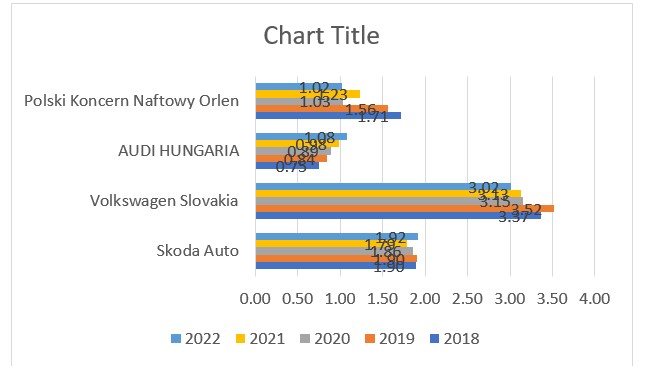

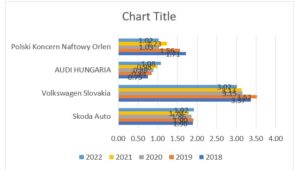

Figure 5 shows the shift in the asset turnover ratio between 2018 and 2022, highlighting the significant decline or increase in the indicators studied, which varied for the companies studied, especially in 2022, as some were able to grow during the crises, while others struggled.

Fig 5. Asset turnover ratio 2018-2020 for the largest V4 companies

Source: Authors’ own work based on annual reports

Despite the progress shown by Volkswagen in 2019, the following year saw a decline. Skoda Auto had a stable performance in 2018-2019, which may explain their relatively smaller decline in 2020 and their growth in 2022, which brings them back to pre-crisis levels. Audi is the only company in our study that has been able to show steady growth in the indicator and period we study. In contrast, the Polish company faced a downturn, exacerbated by the pandemic, with positive growth in 2021, but a fall again in 2022. It is important to consider the impact of the conflict in Ukraine on these companies, as the war disrupted regional stability and economic conditions, which could have further affected their performance. It has also disrupted the recovery from the pandemic period, so in future research, it will be necessary to include this factor as well, as it is a protracted conflict. However, further analysis is needed to assess the specific impact of the war on the asset turnover ratios of these companies.

Discussion

As the world approaches victory over COVID-19, many are beginning to ponder what the post-pandemic future will hold. Will we simply return to life as it was in 2019? Interestingly, we must look back almost a century to find historical parallels, to a time when the world was facing a similar situation. The great pandemic of 1918-19 resulted in millions of deaths, material loss, and confusion. However, after the sudden disappearance of the Spanish flu, a new era of culture and habits began – the “new norm” of the time – which became known as the Roaring Twenties. This unique period after the global pandemic lasted until 1929 and offers us valuable lessons to consider as we move forward. By 1928, the USA had become spectacularly wealthy, but even countries that had suffered heavy losses in the First World War were prospering. There was a sense of optimism as the decade drew to a close, as the shackles continued to be broken and people found more and more opportunities for entertainment, casual mating, and were fascinated by the dizzying pace of progress that had connected people all over the world with aeroplanes and radio waves. But then came the Dirty Thirties, because the Great Depression hit in 1929.

Unfortunately, we cannot ignore the events that occurred in 2022 with the war in Ukraine. The war has caused immense destruction and loss of life, and its consequences are still being felt today. We cannot allow history to repeat itself with a reverse order of events, first the pandemic, then world war. The parallels between the situation nowadays and the situation of the Roaring Twenties are frightening, with people’s propensity to spend leading to inflation figures. However, we can only hope that the situation will improve, and that nations around the world will work together to prevent further conflicts and promote peace.

Conclusion

The epidemic, which started in China in autumn 2019 and will reach and infect the whole world in 2020, has an unpredictable economic impact. However, it is clear that the impact of the pandemic will require a new approach to health and economic crisis management in countries around the world. Each country is implementing its crisis management strategy in a different way, but they all share the common goal of counteracting the socio-economic impact. We do not yet know which strategy will be successful, but we can look to the future with optimism about the success of vaccination. The virus has slowed the economy and there is no sector where the impact of the epidemic is not being felt. The latest figures show that tourism, including accommodation, remains the sector most affected. However, it is not only tourism but also catering and related services that are in serious crisis. The firms we surveyed are not involved in these sectors and are therefore not at high risk.

Several studies have looked at the critical situation in the automotive and construction sectors, where significant job losses have occurred. Disciplined and self-financing economic policies can be an advantage in tackling the crisis, but further measures may be needed until the epidemic subsides and the economy recovers. The epidemic has made it clear that countries’ economies and development are now highly interlinked. Tackling the pandemic can no longer be a country-by-country or national effort. It must be a global effort, with the more resilient countries, which are better able to bear the burden, helping the poorer countries. This has been clearly demonstrated by the need to share vaccines. A good example is the EU’s Next Generation package, an over €800 billion temporary recovery facility to help repair the immediate economic and social damage caused by the coronavirus pandemic. Europe will be greener, more digital, more resilient, and better prepared for the new challenges if they can successfully apply financial support by this way.

References

- Ahmad, A., Jamaludin A., Zuraimi, N. S. M., Valeri, M. (2020), Visit intention and destination image in post-Covid-19 crisis recovery. Current Issues in Tourism Latest Articles 24 (17), 2392-2397.

- Aqeel, M. et al. (2020). The Influence of Illness Perception, Anxiety and Depression Disorders on Students Mental Health during COVID-19 Outbreak in Pakistan: A Web-Based Cross-Sectional Survey. International Journal of Human Rights in Healthcare, 2020, https://doi.org/10.21203/rs.3.rs-30128/v1

- Bajzikova, L., Novackova, D., Saxunova, D. (2017) Globalization in the case of automobile industry in Slovakia. Proceedings of the 30th International Business Information Management Association Conference, IBIMA, 4879-4893.

- Balázs, P. (2020). A COVID-19 válság integrációs hatásai. Köz-gazdaság 15 (2), 5‒12.

- Chen, S., Igan, D., Pierri, N., Presbitero, A. (2020). Tracking the economic impact of COVID-19 and mitigation policies in Europe and the United States. IMF Working Papers No. WPIEA2020125, Washington.

- Czeczeli, V., Kolozsi, P., Kutasi, G., Marton, Á. (2020). Gazdasági kitettség és válságállóság exogén sokk esetén: A Covid-19-járvány rövid távú gazdasági hatása az EU-ban. Pénzügyi Szemle 3: 323‒349.

- Fernandes, N. (2020). Economic effects of coronavirus outbreak (COVID-19) on the world economy. IESE Business School Working Paper No. WP-1240-E.

- Kincses, Á., Tóth, G. (2020). How coronavirus spread in Europe over time: national probabilities based on migration networks. Regional Statistics 10 (2): 228–231.

- Kovács, S. (2020). Települési önkormányzatokat érintő bevételkiesések a járványhelyzetben. Tér és Társadalom 34 (2): 189‒194.

- Lescure, F. X., Bouadama, L., Nguyen, D., Parisey, M., Wicky, P. H., Behili, S., et al. (2020). Clinical and Virological Data of the First Cases of COVID-19 in Europe: a case series. The Lancet Infectious Diseases, 20(6): 697–706.

- AUDI HUNGARIA (2023). Általános üzleti évet záró. [Online]. [Retrieved May 29, 2023]. https://e-beszamolo.im.gov.hu/oldal/kereses_merleglista

- Orlen (2023). Powering the future. [Online]. [Retrieved April 30, 2023] https://www.orlen.pl/en/investor-relations/reports-and-publications/financial-results

- Sevcik, M., Koten, M., Lubor, S. (2020). Failure of European Union institutions in resolving coronavirus crisis and in subsequent redistribution of funds. 13th Economics & Finance Virtual Conference, Prague. ISBN 978-80-87927-95-3

- Škoda. (2023). VÝROČNÍ ZPRÁVA. [Online]. [Retrieved March 31, 2023] https://www.skoda-storyboard.com/cs/vyrocni-zpravy/

- Tamásné, ZS. (2020). A novemberi bruttó bér felét téríti meg az állam a bezárni kényszerülő létesítményeknek, de csak utólag. [Online]. [Retrieved February 22, 2023] https://24.hu/fn/gazdasag/2020/11/11/berkoltseg-tobb-mint-felet-teriti-meg-az-allam-de-csak-utolag/

- (2020). Na ceste k udržateľnosti. [Online]. [Retrieved January 31, 2022] https://sk.volkswagen.sk/content/dam/companies/sk_vw_slovakia/podnik/vyrocne_spravy/Vyrocna_sprava_2020.pdf

- Zhang, Y., Lange, K. W. (2021). Coronavirus Disease 2019 (COVID-19) and Global Mental Health. Glob Health J, 2021, Vol. 5 (1): 31-36, https://doi.org/10.1016/j.glohj.2021.02.004