Introduction

Corporate governance based on rules set by statutory and sub-statutory instruments has proved insufficient in cases of undetected fraud and abuse, described in the literature for many years, leading to numerous bankruptcies. In the face of financial crimes often resulting in the loss of the life’s work of the defrauded shareholders, it became necessary to introduce additional mechanisms to minimise the risk of embezzlement (Stępień, 2013, p.367). Hence the importance of new organisational mechanisms that have been introduced and refined over the years to increase the effectiveness of supervision (Aluchna, Koładkiewicz, 2018, p.12). One example is sets of recommendations – best practices (soft law), the application of which is supposed to improve the functioning of the company, increase its credibility and improve its assessment in the eyes of current or potential investors. Companies listed on the Warsaw Stock Exchange apply the recommendations adopted in the document entitled Best Practices for WSE Listed Companies 2021 (hereinafter referred to as the: BPLC 2021). In the context of improving the effectiveness of supervision, it is particularly interesting to note the attitude of companies to the rules (Aluchna 2009, p.19) specified in the BPLC 2021 document regarding internal systems and functions that allow for ongoing control and mitigation of business risks (Aluchna, 2013, p. 107).

This paper presents the essence of the process of establishing sets of best practices in historical terms. It was followed by an analysis of the information reported by selected WSE listed companies as regards the application or not of rules concerning internal systems and functions. The results of the analysis made it possible to present the position of the managements of the analysed groups of companies on the need to introduce additional independent internal corporate governance mechanisms.

Process of strengthening corporate governance mechanisms

At the same time as the separation of capital ownership from the management function, the owner’s access to information about the company was restricted (information asymmetry). A. Berle’e and G. Means in their book “The Modern Corporation and Private Property”, published in 1932, describe this phenomenon as the so-called “power of managers” (Berle, Means, 1968). It is particularly dangerous given the contradiction between the interests of the owner (principal) and the management (agent) discussed in the literature (Maruszewska, 2015, p.185). This contradiction increases the likelihood of exacerbating information asymmetries (Stępień, 2013, p.375) by manipulating reporting information. In order to prevent fraudulent practices, it becomes necessary for the company to implement both internal and external controls that form a comprehensive system of supervision of its activities in all aspects, broadly referred to as corporate governance.

At this point, it is worth quoting one of the key definitions of H. Baer and C. Gray, according to which corporate governance is a system of “monitoring and control, necessary to gain access to the information necessary to make investment decisions and to monitor agents (managers), to act in the interest of the owners of capital” (Herdan 2007, p. 29). This complex system of safeguards against infringement of the interests of not only the owners of capital anymore but also of other interest groups in the company is consistently subject to processes of evolution. The changes in legal and organisational solutions observed in it result from the need to continuously adapt the system to changing socio-economic conditions. The need for changes in the corporate governance system was first pointed out in a report by Sir Adrian Cadbury published in 1992 as well as in a Canadian report entitled Where were the members of the management boards? The result of the desire to mitigate the threat posed by the perceived inadequacies of the protection system were rules that formed recommendations by institutional investors such as the California Public Employees Retirement System, CalPERS Statement of Governance Rules, 1996 (Czarnecki 2004, p. 441), followed by OECD guidelines (OECD 2015). Despite these regulatory actions, the observed decline in confidence in the effectiveness of the corporate governance system influenced the need for deeper change in the form of reform. In the case of the Great Britain, the guidance documents were adopted in the form of the two reports by Smith and Higgs. In the United States, the revelations of Enron’s years of financial information manipulation, resulting in the spectacular collapse of the company, raised questions about the effectiveness of the supervisory mechanisms in place and the efficiency of the disclosure verification system.

To reduce the risk of similar abuses in the future, the Sarbanes-Oxley Act was adopted in the U.S. Congress in July 2002 (Czarnecki, 2004 p.442). Within the framework of the new restrictive law introduced, the Americans established new institutions for the supervision of companies, imposed a number of new obligations on companies and their bodies, strengthened the power of the Securities and Exchange Commission and defined offences leading to capital market violations, while increasing the severity of penalties imposed for their commission (Czarnecki, 2004, p.443). In the case of the new British regulations, the primary emphasis was on the integrity and independent judgement of the people involved in the corporation. This included, for example, the concept of appointing independent non-executive directors, the use of professional audit committees, transparency also equated with the comply or explain rule (Aluchna, Koładkiewicz, 2018, p.13, Mucha 2016, p.21). Increasing importance was attached to the popularised so-called best practices (Aluchna 2014, s. p. 13).

Best practices (corporate governance codes) as a “soft law” supporting the effectiveness of internal corporate governance mechanisms

The aforementioned best practices are the rules for establishing and applying an effective corporate governance system included in the so-called best practice sets. The organisational solutions specified in them support the effectiveness (Castrillón, Alfonso 2021, p. 181) of the supervision mechanisms used in the entity, including internal corporate governance mechanisms. These regulations were intended to lead to the building of a reputation and a relationship with shareholders based on mutual trust (Żabski 2013, p. 132). The aim of the authors of these studies was to create a system of additional safeguards. The resulting sets of recommendations covered issues concerning the internal and external relations of supervised institutions, including relations with shareholders and customers, their organisation, the functioning of internal supervision and key internal systems and functions as well as statutory bodies and the rules of their interaction. However, it should be emphasised that they formed only sets of promoted recommendations without binding force (Blejer-Gołębiowska, 2012, p. 56) – the so-called “soft law”.

The impetus for their adoption was the fact that, despite the obligations imposed on the management of companies arising directly from the law (“hard law”) including the obligation to maintain information integrity, significant irregularities were occurring resulting in the loss of capital invested by the owners. As early as the 1970s, the development of codes of conduct began.

The first document promoting the rules of corporate governance was the Statement on Corporate Governance, prepared in the United States in 1978 by the Business Roundtable, an association of managers of major American corporations. This document focused on the role and operation of the supervisory board as well as the general meeting of shareholders. The next document was a code prepared 11 years later by the Hong Kong Stock Exchange. In Europe, the first set of indications and recommendations – best practices – was published in 1991 in Ireland (Bogacz-Miętka, 2011 p.118). Nevertheless, Great Britain is considered to be the forerunner of the introduction of this type of regulation in Europe. Thus, after the publication of the Cadbury Code document in Great Britain in 1992 (Aluchna, 2008, s.18, Jeżak, 2002, p.3), a number of other studies based on it appeared worldwide, and the emerging sets were also subject to periodic revision and amendment resulting in the introduction of further revised documents (Cuomo, Mallin, Zattoni, 2018).

The sets of the so-called best practices currently in use are essentially based on the solutions adopted in a document prepared in 1999 and updated in subsequent years by the OECD (OECD, 2004, Jeżak, 2002, p. 4). However, the rules adopted by the OECD do not have the character of a binding act of international law. They are therefore an excellent example of the so-called “soft law” (Oplustil, 2010 p.60-61).

The underlying concept for their authors was that ensuring effective and efficient supervision increases confidence in the organisation, as only effective supervision acts as a barrier against irregularities. This increases the likelihood of an entity’s financial stability as well as the chance of an increase in its value. The most popular European sets of rules – best practices – which, however, had their origin in the rules adopted by the OECD, are the following (Bogacz-Miętka, 2011, p.129):

- Euroshareholders (European Shareholder Group),

- EASD (European Association of Securities).

The code of best practices introduced and applicable in Poland, the so-called Best Practices for WSE Listed Companies, was of course also based on the solutions applied in the document developed by the OECD. Initially, the initiative to create a set of best organisational solutions was taken by two organisations, i.e.:

- Polish Corporate Governance Forum operating at the Institute for Market Economics,

- Corporate Governance Forum established by the Business Development Institute (Aluchna, 2008, p.21, Bogacz – Miętka, 2011, p. 132).

A set developed by the latter organisation, Best Practices for Public Companies, hereinafter referred to as the Warsaw Code, was recognised as the leading document and subsequently adopted by the Warsaw Stock Exchange in September 2002 (Aluchna, Koładkiewicz, 2018, p.13). These rules are referred to in the literature as the so-called “soft law” (Gad 2019, p.39). Since January 2003, the issuers of securities have been required to publish annually a statement on the application of the rules indicated in the aforementioned document. Whereby, as in the case of the aforementioned OECD rules, a “comply or explain” solution was originally applied here, requiring the issuer to explain the reasons only for not applying the specified rule (Koładkiewicz, 2014, p.194). Over many years of searching for the best organisational solutions to ensure a high degree of efficiency and safety in the organisation’s operations, the best practices originally adopted have been subject to numerous modifications (Aluchna, 2013, p. 106, Koładkiewicz, 2014, p. 195). In July 2021, after extensive consultations, a new document “Best Practices for WSE Listed Companies 2021 – BPLC 2021(abbreviated)” came into force. It took into account numerous comments made by market participants. One of the key differences between the previously applicable rules and the current rules is the move away from reporting only the fact that a rule is not applied for the benefit of imposing an obligation to publish comprehensive information on the scope of the rules applied. A report on the application of the rules is made available in the form of a form in the Electronic Information Base – reporting system (hereinafter referred to as the: EBI). Analogous to the previous versions of the document, it is divided into six chapters.

The rules of conduct included in BPLC 2021 cover the information, control, motivation and organisational areas. According to the adopted assumptions, the implementation of the rules, understood as the implementation and application of the recommended detailed solutions, is to result in the strengthening of the position of the company’s stakeholders. It should be emphasised that the mere thoughtless implementation of specific organisational solutions does not guarantee their effectiveness. It is, however, the first step towards strengthening corporate governance.

Internal systems and functions are a set of internal corporate governance mechanisms that significantly strengthen internal supervision of the company. A key role is assigned here to the internal audit function monitoring and reporting on the effectiveness of internal control systems in all areas of the company’s operations (Wróbel 2013). The organisational independence of internal audit is a key attribute that enables an independent and objective assessment of the effectiveness and efficiency of the company’s control mechanisms and the subsequent formulation of recommendations to improve the system.

Assessment of the level of using internal corporate governance mechanisms on the basis of reports on the application of the BPLC 2021 rules – selected issues

In order to ensure greater transparency and increase the scope of information allowing for a correct assessment of the company’s collateral, the Warsaw Stock Exchange in 2021 changed the manner in which the obligation to report and present the level of implementation of the rules specified in the document dedicated to companies listed on the WSE is implemented. The methods of making available the information from these reports have also been changed. This has provided investors with a source of valuable information to better assess investment risks. An analysis of the WSE reports made available on the application of the rules of the BPLC 2021 provides a basis for assessing the attitude of the company’s management to the concept of strengthening internal supervision by, among other things, introducing independent units into the organisational structure to monitor the correctness of the functioning and recommend ways to improve the collateral system. Since July 2021, following the adoption by the WSE of the updated set of best practices for WSE listed companies, the companies fulfilling the obligation to report the application of the rules specified in BPLC 2021 have been filling in the form made available to them in the EBI system. As a result, collecting and then presenting information on the implementation of the rules in a structured manner has become easier and also more effective. Moreover, the use of a single unified template now allows for multi-variant benchmarking between companies and their groups.

In order to facilitate market participants’ access to information about the company in the context of its compliance or non-compliance with best practice rules, the WSE has made available a new tool, the Best Practice Scanner. It operates “solely on the basis of information provided via the EBI system by listed companies pursuant to § 29 section 3 of the WSE Rules, hence the scope of data presented in the Best Practice Scanner is a reflection of the aforementioned information published by companies” [1].

Using the information entered by companies in the EBI system, presented through the scanner, the following reviews selected groups of companies in terms of the application of the rules listed in the BPLC 2021 document.

The basis of the analysis was an attempt to answer the question to what extent companies comply with the promoted solutions strengthening their internal corporate governance mechanisms and which rules are applied to a limited extent or are not applied at all by the companies. In analysing the data available, it was assumed that companies reliably report the status of implementation and application of rules forming best practices of the WSE listed companies.

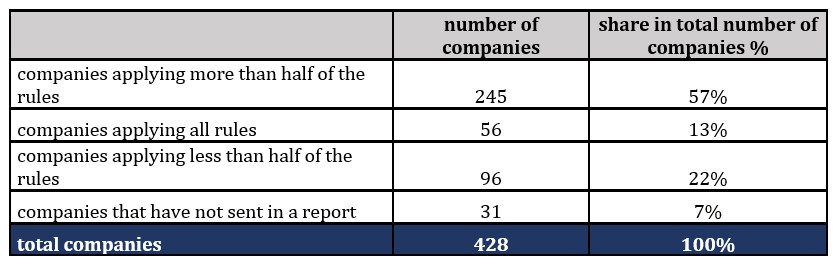

On the basis of the analysis of data collected in 2021 using the best practices scanner, it was found that out of all WSE listed companies, 31 did not fulfil their reporting obligation which represents 7% of the total number of companies covered by the analysis. More than half of the examined entities reported applying more than half of the rules, while 22% of the analysed companies confirmed the implementation of less than half of the recommended organisational solutions. The level of non-reporting of the application of best practices is certainly influenced by the fact that reporting through the EBI system is a new solution introduced with the adoption of BPLC 2021.

Table 1. Application of BPLC 2021 rules – companies listed on the Warsaw Stock Exchange

Prepared by the author based on the best practices scanner (https://www.gpw.pl/dpsn-skaner [accessed 27.11.2021]).

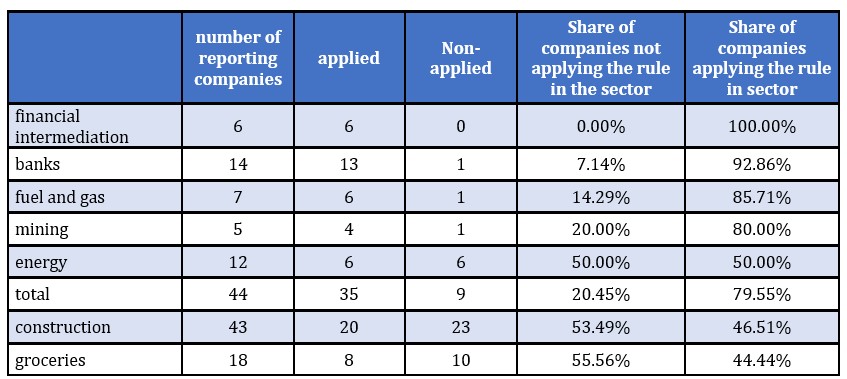

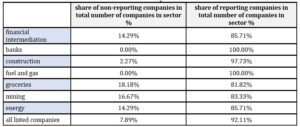

After the assessment of the overall level of fulfilment of reporting obligations, an analysis of selected companies grouped into seven sectors was carried out, including mining, construction, banks, financial intermediation, energy, fuel and gas and groceries. The analysis found the highest level of discipline in the “banks” and “fuel and gas” groups where reports were sent by all entities included in these groups. The highest rate of non-reporting companies was found in the “groceries” group.

Table 2. Reporting on the application of the BPLC 2021rules by selected business sectors – summary

Prepared by the author based on the best practices scanner (https://www.gpw.pl/dpsn-skaner [accessed 27.11.2021]).

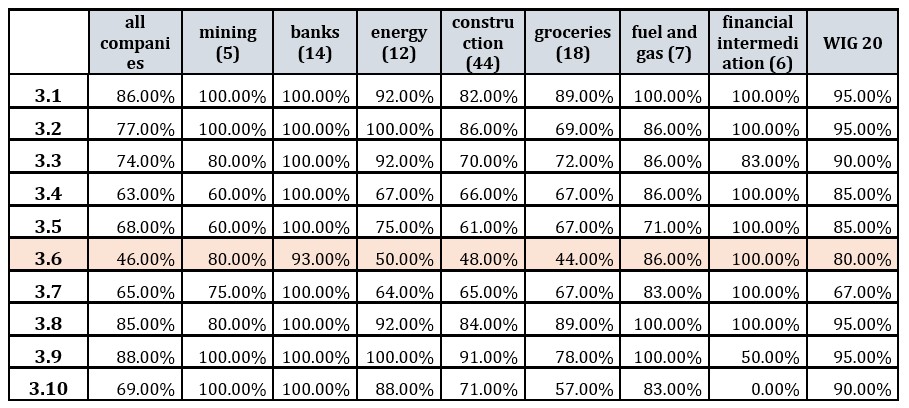

In analysing the implementation of the disclosure obligations related to the application of the BPLC 2021, attention was focused on Rule III (Internal systems and functions) which promotes the appropriate design and use of internal corporate governance mechanisms, i.e., internal control, compliance and risk management systems as well as the internal audit function. Table 3 presents the specific rules the application of which supports the implementation of General Rule 3, according to which: Efficient internal systems and functions are an indispensable tool for the supervision of the company. These systems cover the company and all areas of its group that have a significant impact on the company. It is assumed that the implementation of the solutions described herein has a significant effect on strengthening the internal control system which is intended to reduce the risk of irregularities and consequently protect the owner from the risk of losing the invested capital.

Table 3. Rule III of the BPLC 2021– Internal systems and functions

Source: Best Practices of Companies Listed on the WSE 2021, pp. 10-11 (https://www.gpw.pl/dpsn-skaner [accessed 27.11.2021]).

Taking into account the identified sectors of activity, the level of implementation of all specific rules strengthening the effectiveness of the application of Rule III was assessed. On the basis of the results of the conducted observations, the sectors with the highest and the lowest discipline in the application of the recommended organisational solutions were singled out from among the analysed groups of enterprises, and the detailed recommendation with the lowest level of implementation was indicated. Subsequently, the explanations of selected companies not applying the detailed rule in question were analysed. When assessing the level of implementation of the separate Rule, only companies reporting the application of the BPLC 2021 recommendations were taken into account.

In the assessment of the implementation rate of Rule 3 established as the average level of implementation of specific rules by selected sectors of companies’ activity, it was found that the highest level of its application is demonstrated by the banks sector (99.30%), followed by the fuel and gas sector (88.10%). It is higher than the average application of Rule 3 reported by all companies (72.10%) and the WIG 20 average (87.70%). The lowest level of application is shown by companies in the food and construction sector.

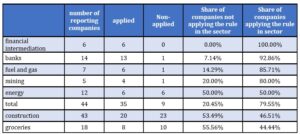

Table 4: Share of companies applying an isolated detailed rule in the total number of reporting companies in the group (excluding companies that have not sent a report) by selected sectors

Prepared by the author based on the best practices scanner (https://www.gpw.pl/dpsn-skaner [accessed 27.11.2021]).

On the basis of the data analysis specified in the table above (Table 4), it can be concluded that specific Rule 3.6, relating to the organisational and functional subordination of the head of internal audit, is one whose application is limited in many cases. The application rate for all companies is only 46%. This Rule shows the lowest rate of application in relation to the other nine specific rules in the banking, energy, construction and groceries sectors. In the mining and oil and gas sectors, a lower application rate is found for rules 3.5 and 3.7, which also refer to the independence of control functions resulting from the location of the managers of the activities that constitute internal corporate governance mechanisms.

Table 5 presents the results of the detailed analysis carried out of the application reports of the DBSN 2021 rules in terms of the implementation of all the specific rules that constitute solutions for the full implementation of Rule 3 – internal systems and functions. Indicators of the level of responses confirming the application or non-application of the Rule are presented here. The analysis covered all reporting companies, WIG 20 companies and selected groups of companies grouped according to the aforementioned sectors of activity.

Table 5 Level of application of specific Rule 3.6 – Internal systems and functions – by selected sectors of activity

Prepared by the author based on the best practices scanner (https://www.gpw.pl/dpsn-skaner [accessed 27.11.2021]).

Table 6 below presents the explanations of companies that do not apply Rule 3.6. The entries in the form submitted to the EBI system often indicate a lack of understanding of the role of internal audit, the main attribute of which should be independence allowing objectivity to be maintained.

Table 6 Explanation of companies not applying Rule 3.6

Prepared by the author based on the best practices scanner [https://www.gpw.pl/dpsn-skaner access: 21.11.2021 r.]

Conclusions

The importance of applying appropriate organisational solutions in the area of internal systems and functions which form an important mechanism of corporate governance is confirmed by the position of the authors of BPLC 2021. In the light of a number of financial scandals confirming the far-reaching “imperfection” of reporting processes, it is advisable to strengthen internal control mechanisms. No less important is also the introduction of an independent function into the organisation – internal audit, reporting directly to the company’s supervisory board. The purpose of ensuring the full independence of the internal auditor is to reduce the risk of being influenced and pressured not only by the audited employees but also by the management board itself. Only in this way is it possible to maintain objectivity in the assessment of the processes under review. The lack of implementation of best practice in this respect and the assignment of this function to the executive director – the Management Board or the assignment of additional tasks to a person responsible for another area makes it impossible to carry out tasks in accordance with the International Standards for the Principles for the Professional Practice of Internal Auditing (2016). In this situation, it is difficult to describe internal audit as a corporate governance mechanism that effectively counteracts the risk of irregularities, including reporting irregularities. The tool made available by the Warsaw Stock Exchange – the best practice scanner – makes it possible to observe the actual application by companies of solutions aimed at protecting the interests of the owner and other stakeholders. The analysis carried out above shows that it is often difficult for the management board (agent) to see the role played by the internal auditor in an independent assessment of the internal control system as positive. This function is intended to significantly reduce the adverse impact and effects of the phenomenon of information asymmetry. With the new reporting formula for the implementation of the BPLC 2021, it will be possible to observe changes in these trends in the near term.

List of tables

Table 1. Application of BPLC 2021 rules – Warsaw Stock Exchange listed companies

Table 2. Reporting on the application of the BPLC 2021 rules by selected business sectors – summary

Table 3. Rule III of the BPLC 2021 – Internal systems and functions

Table 4. Share of companies applying a separated detailed rule in the total number of reporting companies in the group (excluding companies that have not sent a report) by selected sectors

Table 5. Level of application of specific Rule 3.6 – Internal systems and functions – by selected sectors of activity

Table 6. Explanation of companies not applying Rule 3.6 – The person in charge of internal audit reports organisationally to the President of the Management Board and functionally to the chairman of the audit committee or to the chairman of the supervisory board if the board acts as an audit committee.

References

- Aluchna M. (2008) Dobre praktyki corporate governance. Światowe tendencje a polskie doświadczenia [in]: e-mentor 2 (24), SGH,18-25, [Online}, [Retrieved 13.09.2022] www.e-mentor.edu.pl

- Aluchna M. (2013) Dobre praktyki spółek notowanych na GPW w Warszawie. Analiza zmian wprowadzonych w latach 2010–2012 [in]: Studia I Prace, Kolegium Zarządzania i Finansów, Zeszyt Naukowy 132,Warsaw, 105-130.

- Aluchna M. Koładkiewicz I., Dobre praktyki ładu korporacyjnego. Perspektywa Rady Nadzorczej., Organizacja i Kierowanie, 3/2018 (182), 11-31.

- Aluchna M. (2009), Nadzór korporacyjny Współczesne tendencje Wyzwania dla Polski. Przegląd Organizacji, Nr 10 (837), TNOiK, 16-20.

- Aluchna M. (2014), Nadzór korporacyjny wobec krytyki koncepcji shareholder value, Studia Prawno- Ekonomiczne, Vol. XCI/2, 9-24.

- Berle, A., Means, G. (1968). The modern corporation and private property, New York.

- Dobre praktyki spółek notowanych na GPW 2021 (2021), GPW [online], [Retrieve 15.09.2022], https://www.gpw.pl/pub/GPW/files/PDF/dobre_praktyki/DPSN21_BROSZURA_wersja_do_druku.pdf

- Blejer-Gołębiowska A. (2010), Asymetria informacji w relacjach inwestorskich. Perspektywa nadzoru korporacyjnego, Wydawnictwo Uniwersytetu Gdańskiego, Gdańsk.

- Bogacz- Miętka O. (2011), Kompendium wiedzy o nadzorze i kontroli nad przedsiębiorstwem, CEDEWU.pl

- Castrillón G., Alfonso M.(2021), The concept of corporate governance, Scientific Journal “Visión de Futuro”, vol. 25, no. 2. National University of Misiones, Argentina, 76-88, [Online], [Retrieved 15.09.2022] https://www.redalyc.org/articulo.oa?id=357966632010

- Cuomo F. Mallin Ch., Zattoni A. (2018), Corporate governance codes: A review and research agenda, Corporate Governance: An International Review cumo2016, Vol. 24 (3), 222-241.

- Czarnecki J.S. (2004), Polski ład korporacyjny – trzecia droga [w]: Ekonomiczne i społeczne problemy nadzoru korporacyjnego, ed. Rudolf S., Wydawnictwo Uniwersytetu Łódzkiego, 441-458.

- Gad J. (2019), Mechanizmy ładu korporacyjnego a system kontroli nad sprawozdawczością finansową, Wydawnictwo Uniwersytetu Łódzkiego, Łódź.

- Herdan, A., (2007), Przesłanki i warunki funkcjonowania nadzoru korporacyjnego, Zeszyty Naukowe Wyższej Szkoły Ekonomicznej w Bochni nr 6, Wydawnictwo Wyższej Szkoły Ekonomicznej w Bochni, Bochnia, 27-45.

- Jeżak J. (2002), Nadzór korporacyjny – kodeksy dobrych praktyk. Przegląd Organizacji, 5/2002, TNOiK, 3-8.

- Koładkiewicz I. (2014), Dobre praktyki ładu korporacyjnego oraz ich transfer do twardego prawa. Perspektywa interesariuszy polskiego rynku kapitałowego, Studia Prawno-Ekonomiczne, vol. XCI/2, 193-212.

- Maruszewska E.W. (2015), Etyczne aspekty zarządzania z punktu widzenia rachunkowości w świetle teorii agencji oraz teorii interesariuszy, Zeszyty Naukowe Politechniki Śląskiej, Organizacja i Zarzadzanie (79), 179-190.

- Mucha A. (2016) Dobre Praktyki Spółek Notowanych na GPW 2016 – kontynuacja czy rewolucja? [in]: Allerhand Working Paper 15/2016, Instytut Allerhanda, Kraków, [Online], [Retrieved 15.09.2022]

- https://www.researchgate.net/publication/296678957_Dobre_Praktyki_Spolek_Notowanych_na_GPW_2016_-_kontynuacja_czy_rewolucja

- OECD (2015), G20/OECD Principles of Corporate Governance, OECD Publishing, Paris [Online], [Retrieved 15.09.2022], http://dx.doi.org/10.1787/9789264236882-en

- Oplustil K. (2010), Instrumenty nadzoru korporacyjnego (corporate governance) w spółkach akcyjnych, Warszawa.

- Principles for the Professional Practice of Internal Auditing (2016), The institute of internal auditors, Florida USA [Online], [Retrieved 27.12.2022] https://www.theiia.org/en/standards/what-are-the-standards/core-principles/

- Stępień M. (2013), Ndzór korporacyjny a teoria agencji, Zeszyty naukowe Wyższej Szkoły Bankowej w Poznaniu, Poznań. Vol.49 no.4, 367-377.

- Skaner dobrych praktyk (2021), GPW. [Online], [Retrieved15.09.2022] https://www.gpw.pl/dpsn-skaner

- Wróbel A. (2013), Kontrola wewnętrzna i audyt wewnętrzny jako niezależne narzędzia wspierające realizację celów przedsiębiorstwa, [Online], [Retrieved 27.12.2022] https://grantthornton.pl/publikacja/audyt-wewnetrzny-i-kontrola-wewnetrzna-jako-niezalezne-narzedzia-wspierajace-realizacje-celow-przedsiebiorstwa/

- gpw.pl/dpsn-skaner [Retrieved 27.11.2021] .

- Żabski Ł. (2013), Kodeks dobrych praktyk jako narzędzie doskonalenia nadzoru korpo-racyjnego, „Prace Naukowe Akademii im. Jana Długosza w Częstochowie”, vol. VII, 127-141.