Introduction

Over the last decade, the world has witnessed the tremendous growth of the telecommunication industries which has resulted in the use of cell phone or mobile phone by almost all ranks of people. Today, the use of cell phone has become almost inevitable as its usage has infused into all spheres of human activities, from personal entertainment to doing monetary or business transactions. Just as the intensity of scientist investigating on advancing and sophisticating the mobile technologies, scholars and researchers alike have also been very active in studying the social aspect of the mobile usage. One of the most popular topics which has received much interest among IS researchers is the aspect of trust in using the mobile banking. Soderstrom (2009) defined trust as the willingness to believe in the reliability, honesty, dependability and capability of others; and hence also to be vulnerable to the actions of others [32]. There are two main actors in trust: the trustor i.e. the trusting party, and the trustee which is the trusted party.

In the context of mobile banking, the trustor would be the consumer of mobile banking services while the trustee would cover not only the retail banking that provides the mobile banking services but also the mobile telecommunication provider and the mobile telephone technology itself. The extant literature on the aspect of trust in mobile banking shows that most studies have been focusing on the retail banking and the mobile telecommunication provider only. McKnight et al. argue that trust in technology is equally important in ensuring successful adoption of services rendered through the technology itself. Considering that very few studies have actually addressed the aspect of trust with all the three categories of trustee i.e. the retail banks, the mobile telecommunication provider and the mobile telephone in one single study, this study attempts to address this gap. In particular, empirical study focusing on trust in mobile banking involving Malaysian consumers is also still very scarce. Against this background, this study is proposed with the aim of examining trust in mobile banking. Based on the extensive review of the literature, this paper develops a conceptual model on trust in mobile banking.

Literature Review

Trust

According to Belanger & Carter (2008), trust has been explored extensively and defined differently in numerous research studies. Soderstrom (2009) identifies 29 different types of trust, all of which are somewhat different, and relating to each other in a variety of ways. Accordingly, Soderstrom (2009) categorizes trust into three categories of trustee namely, organization, person and technology. For each category, it is further subdivided into two, which are knowledge-based trust and cognitive-based trust which are experienced by the trustor or consumer. Organization or institution-based trust focuses on relying upon an institution or third party to build trust (Gefen et al., 2003). Person or personality-based trust refers to individual personalities that influence trust building. Technology trust relates to an individual’s willingness to be vulnerable to an information technology based on expectations of technology predictability, reliability and utility (Lippert & Davis, 2006). Knowledge-based trust which is also known as experienced trust is about trust building through repeated interactions. In other words, the trustor must engage in repeated interaction over a longer period of time with the trustee and in the process, trust is developed. On the other hand, cognitive-based trust which is also termed as initial trust, refers to trust building through first impression rather than repeated interactions.

Mobile Banking

The internet has evolved from its fixed line constraints and is increasingly mobile. Mobile phone handsets, which were initially used almost exclusively for voice calls are now often used for banking transactions. Drexelius & Herzig (2001) defined mobile banking as the ability to conduct bank transactions via a mobile device, or more broadly to conduct financial transactions via a mobile terminal. On the other hand, Barnes & Corbitt (2003) defined mobile banking as “a channel whereby the customer interacts with a bank via mobile device, such as a mobile phone or personal digital assistant (PDA)”. Mobile banking services can be classified based on the originator of a service session, either “push” or “pull” (Infogile Technologies, 2007). ‘Push’ is when the bank sends out information based upon an agreed set of rules; for example, the banks send out an alert when the account balance goes below a threshold level. On the other hand, ‘Pull’ is when the customer explicitly requests a service or information from the bank, for instance requesting the last five transactions statement. The other way to categorizing the mobile banking services is based on the kind of services, either transaction-based or enquiry-based (Infogile Technologies, 2007). A request for the bank statement is an example of enquiry-based service while a request for our fund’s transfer to some other account is an instance of transaction-based service.

According to Infogile Technologies (2007), presently, mobile banking is being deployed using mobile applications developed on one of the following four channels: (i) IVR (Interactive Voice Response), (ii) SMS (Short Messaging Service), (iii) WAP (Wireless Access Protocol) and (iv) Standalone Mobile Application Clients. The IVR or Interactive Voice Response service operates through pre-specified numbers that banks advertise to their customers, and the customers can choose options by pressing the corresponding number in their keypads and the corresponding information are then read out, mostly using a text to speech program. The SMS will require the customer to send an SMS containing a service command to a pre-specified number and the bank will respond with a reply SMS containing the specific information. The WAP uses a concept similar to that used in Internet banking where the banks maintain WAP sites which customer’s access using a WAP compatible browser on their mobile phones. Standalone mobile applications clients provide the most comprehensive banking transactions as customers can customize the user interface complexity supported by the mobile.

Mobile banking offers many benefits and advantages to not only customers or users, but also to the telecommunication providers and financial institution that provides the services. Goswami & Raghavendran (2009) note that based on best practices in mature mobile-banking markets, the advantages of mobile banking to end-users include: (i) secure authentication, transaction and data transmission, and easy deleting of content in event of handset loss; (ii) icon-driven, user-friendly interface; (iii) contactless payment that offers quicker checkout at the point-of-sale and replaces all current payment solutions; (iii) dynamic credit facility and innovative point-of-sale offers; (iv) dynamic account monitoring and around-the-clock alerts; (v) convenience of micro-payments (parking meters, vending machines); (vi) real-time access to account information, outstanding debt and bill payment; (vii) ubiquitous access to banking services (personal ATM). With mobile banking, telecommunication providers can expand their services portfolio, promote their brands and create strategic marketing differentiation, hence attracting new customers (Gemalto, 2011). Mobile banking also increases telecommunication providers’ revenue by providing subscribers with instant access to airtime purchase, hence increasing traffic. In addition, with financial services at their fingertips, mobile users will conveniently recharge their prepaid accounts or pay their post-paid bills. In terms of the benefits to the mobile banking provider, mobile banking enhances customer satisfaction and retention by offering new and better services and at the same time provides a direct marketing channel for their products and services, which can be customized to the specific needs of customers. Having mobile phones as the ATMs for their banking services at anytime and from anywhere also generates revenue through higher service usage and reduces operating expenses (Gemalto, 2011).

Mobile Banking in Malaysia

A recent survey by InMobi (2011), the world’s largest independent mobile ad network, found that out of 1,091 Malaysians, 57 per cent of the respondents primarily or exclusively accessed the web via their mobile devices. The study also revealed that the mobile was the top media choice for Malaysians using the web, and mobile banking in particular was expected to increase all across demographics. In Malaysia, as of January 2012, the banks that offer mobile banking are Al Rajhi Banking & Investment Corporation (Malaysia) Berhad, AmBank (M) Berhad, Bank Islam Malaysia Berhad, Bank Simpanan Nasional, CIMB Bank Berhad, Citibank Berhad, Hong Leong Bank Berhad, Malayan Banking Berhad, OCBC Bank (Malaysia) Berhad, Public Bank Berhad, RHB Bank Berhad and Standard Chartered Bank Malaysia Berhad (Central Bank of Malaysia, 2012). Attempts to investigate mobile banking adoption among Malaysian consumers have been reported in the extant literature (Goswami & Raghavendran, 2009; Gu etal., 2009). Daud et al. (2011) examined critical success factors that influence the adoption of mobile banking in Malaysia using extended Technology Acceptance Model (TAM). Based on the responses of 300 banking users, the study found that perceived usefulness, perceived credibility and awareness about mobile banking have significant effect on user’s attitude, thus influencing the intention toward mobile banking. In another study, Cheah et al. (2011) also investigated the factors that influence Malaysians’ intention to adopt mobile banking by extending the renowned framework of Technology Acceptance Model (TAM). Factors such as perceived usefulness (PU), perceived ease of use (PEOU), relative advantages (RA) and personal innovativeness (PI) were found positively related to the intention to adopt mobile banking services. While the aforementioned studies have helped to increase our understanding of mobile banking adoption behavior in Malaysia, these studies however did not address the issue of trust. Kim et al. (2009) and Lee & Chung (2009) note that the lack of trust is one of the most frequently cited reasons for customers not using mobile banking.

Related Studies on Trust in Mobile Banking

Unlike trust in e-commerce or m-commerce which has been quite extensively researched, studies on trust mobile banking is still very limited. Adapting the Delone & Mclean model (1992), Lee & Chung (2009) studied factors influencing trust in mobile banking involving 276 consumers in Korea. The findings showed that predictors of trust in mobile banking are information quality, system quality and interface design quality. The findings also suggest that trust is an important predictor to mobile banking satisfaction. In another study also conducted in Korea, it was discovered that situation normality, structural assurance and calculative-based trust are determinants of trust in mobile banking (Gu et al., 2009). A recent study conducted in China identifies the factors affecting initial trust in mobile banking (Zhou, 2011). The study focuses on the web technology and the mobile banking provider as the trustee. Building upon the information systems success model developed by Delone & Mclean (1992), the study discovered that information quality and systems quality significantly predict initial trust in mobile banking. In addition, it was also found that structural assurance and trust propensity of the trustor significantly predict initial trust. Lin investigated the contribution of knowledge-based trust measured in terms of competence, benevolence and integrity in mobile banking adoption in Taiwan (Lin, 2011). The findings confirmed that all the three knowledge-based trust constructs are predictors of mobile banking adoption.

Conceptual Framework

Mining the literature unveiled that researchers on trust have developed various models for studying the topic. The model on trust developed by McKnight & Chervany (2002) is considered one of the strongest and recognized models as it has been referred to or cited by more than 700 articles. The model which was developed based on the analysis from 65 books and articles on trust from the fields of psychology/social psychology (23), sociology/economics/political science (19) and either management or communications (23). The model which is also known as a typology of trust combines both psychology and sociology fields. According to McKnight & Chervany (2002), because psychologists and sociologists think of the world very differently, their concepts also differ, primarily in terms of the nature of the research behind their origin. Within the model, disposition to trust comes primarily from trait psychology while the institution-based trust derives from sociology. Disposition to trust refers to “the extent to which one displays a consistent tendency to be willing to depend on others in general across a broad spectrum of situations and persons” (2002). Disposition to trust does not necessarily mean that one believes others to be trustworthy but one tends to be willing to depend on others. Institution-based trust signifies that one believes favorable conditions are in place that are conducive to situational success in an endeavor or aspect of one’s life. This construct originates from the sociology tradition that people can depend on others because of structures, situations, or roles that provide assurances that things will go well. In the Internet environment, institution-based trust or “favorable conditions” relates to the legal, regulatory, business and technical environment perceived to support success. According to McKnight & Chervany (2002), trusting beliefs means that: the trustor believes the other party i.e. the trustee has one or more characteristics beneficial to oneself. It also means that the trustor is willing to depend on, or intends to depend on, the trustee even though one cannot control the trustee. In terms of characteristics, the trustor expects the trustee to be willing and able to commit to the consumer’s interest, honest in transactions, and both capable of, and predictable to, delivering as promised. McKnight & Chervany (2002) further elaborated that trusting intentions definitions consist of three elements synthesized from the trust literature, namely: (i) a readiness to depend or rely on another, (ii) trusting intentions is person-specific, and (iii) trusting intentions involves willingness that is not based on having control or power over the other party.

As noted by Soderstrom (2009), trust in technology has also been studied by researchers. According to McKnight et al., in order to gain a more nuanced view of trust’s implications for IT use, MIS research needs to examine how users’ trust in the technology itself relates to value-added post-adoption use of IT (McKnight et al., 2011). By focusing on the technology itself, trust researchers can evaluate how trusting beliefs regarding specific attributes of the technology relate to individual IT acceptance and post-adoption behavior. In this connection, McKnight et al. (2011) applied the trust typology model to study trust in specific technology.

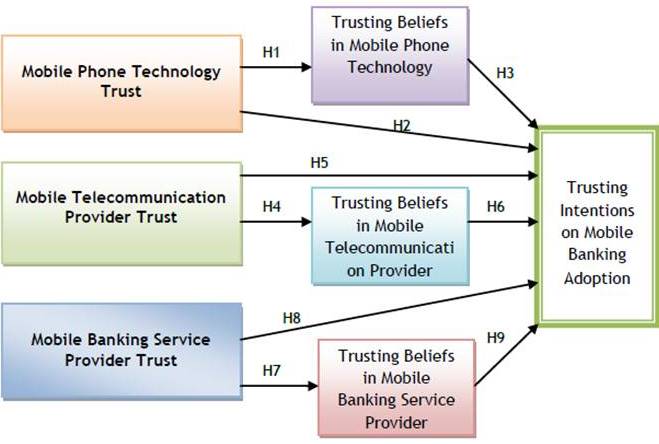

Koo & Wati (2010) define trust in mobile banking as the belief that allows individuals to willingly become vulnerable either to the bank or e-banking technology after having taken the bank’s characteristic embedded in its technology artifact. They argued that this definition captured both traditional view of trust in “a specific party” and trust in “the integrity of technology artifact”, where its process is built the same way as trust in people. Adapting the definition by Koo & Wati [19], the researchers herein define trust in mobile banking “as the belief that allows individuals to willingly become vulnerable to the bank, the telecommunication provider and the mobile technology after having taken the bank’s and the telecommunication provider’s characteristic embedded in the technology artifact”. Figure 1 depicts the proposed framework for studying antecedents and impacts of trust in mobile banking. The framework was developed based on the work of McKnight & Chervany, (2002); McKnight et al. (2002); Meng, Min & Li (2008); Min, Meng, Zhing, (2008); Lu et al. (2011) and McKnight et al. (2011). The constructs of the framework are based on the three categories of trustees, namely the mobile phone technology (i.e. the gadget such as smart phones used by the trustee to engage in mobile banking transactions), the mobile telecommunication provider and the mobile banking provider (i.e. the retail bank that provides the mobile banking services). Consumer trust in these three categories of trustee would lead towards adoption of the mobile banking services.

Figure 1: Conceptual Model on Trust in Mobile Banking

Trusting Intentions in Mobile Banking

Based on McKnight & Chervany (2002), the trusting intention construct is divided into two sub-constructs, which are ‘willingness to depend’ and ‘subjective probability of depending’. As depicted in the conceptual framework, antecedents of the trusting intentions on mobile banking adoption are the trusting belief of the customers’ which are divided into mobile phone technology, mobile telecommunication provider and mobile banking provider. Thus, mobile subscribers who have trusting beliefs in the competence, integrity, predictability and intent of the three groups of trustees are more likely to show willingness to depend on the trustee. According to Dobing (1993), willingness to depend means that an individual out of his own independent accord, is ready to be vulnerable to the other party in a situation by depending on that party. The second sub construct which is the ‘subjective probability of depending’ is the extent to which one anticipates dependence on another party. It also means that the trustor predicts that they will rely or depend on the trustee in the future McKnight & Chervany (2002)

Mobile Phone Technology Trust

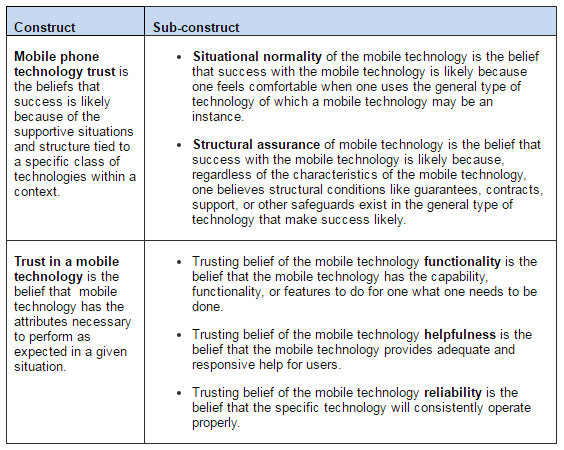

According to Montague (2010), researchers in consumer studies, psychology, engineering and information systems have looked at trust relationships between users and technologies. McKnight et al. (2011) argue that in order to gain a more nuanced view of trust’s implications for IT use, MIS research needs to examine how users’ trust in the technology itself relates to value-added post-adoption use of IT. By focusing on the technology itself, trust researchers can evaluate how trusting beliefs regarding specific attributes of the technology relate to individual IT acceptance and post-adoption behavior. In this connection, McKnight et al. (2011) have applied the trust typology model to study trust in specific technology. Others have showed that trust in technology is critical to mobile banking adoption (Meng etatl. 2008; Min et al. 2008). Based on McKnight et al. (2011), mobile phone technology trust is composed into situational normality and structural assurance, while trusting beliefs of mobile phone technology is divided into functionality, helpfulness and reliability. The description of the construct and sub-construct of mobile phone technology trust is shown in Table 1. The findings of McKnight et al (2011), show that both technology trust and trusting beliefs in technology have a positive relationship with trusting intentions. In addition, technology trust is also found to have significant relationship with trusting belief in technology. To this effect, this study posits that:

P1: Mobile phone technology trust is positively correlated to trusting beliefs in mobile phone technology

P2: Mobile phone technology trust is positively correlated to trusting beliefs in trusting intention in mobile banking adoption

P3: Trusting beliefs in mobile phone technology is positively correlated to trusting intention in mobile banking adoption

Table 1: Definition for Mobile Technology Trust Constructs

Mobile Telecommunication Provider Trust

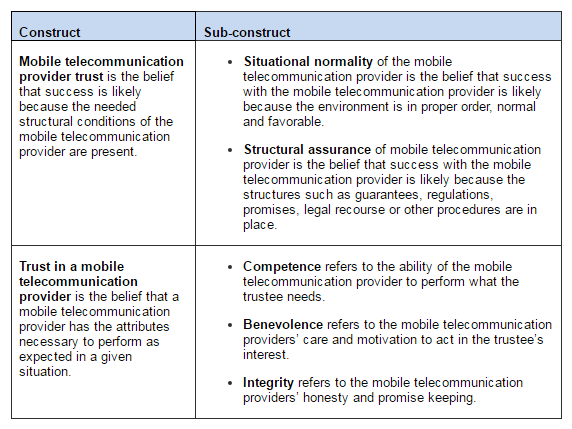

Bangens & Soderberg (2008), stress that the importance of mobile telecommunication provider or telcos in mobile banking should not be underestimated as they are controllers of the mobile telephone networks. Several studies done in Malaysia have shown the importance of service quality in ensuring customer continuous adoption and loyalty to the mobile telecommunication provider (Rahman et al., 2011). Sharma & Ojha (2004) discovered three important factors that determined customer satisfaction of the mobile services, which are network base service performance, retailer-related process performance and network operator related performance. In earlier study involving cellular phone customers in Hong Kong, it was found that transmission quality and coverage of network are the most important factors in ensuring satisfaction (Woo et al, 1999). Other studies showed the importance of the service quality provided by the mobile telecommunication provider in establishing trust in mobile banking (Meng et al., 2008; Min et al., 2008). Institution-based trust, which in this context is the mobile telecommunication provider, predicts both trusting belief and trusting intention; and trusting belief predicts trusting intention (McKnight et al., 2002). The definition for the constructs and sub-constructs of the mobile telecommunication provider trust is given in Table 2. Accordingly, this paper formulates the following prepositions:

P4: Mobile telecommunication provider trust is positively correlated to trusting beliefs in mobile telecommunication provider

P5: Mobile telecommunication provider trust is positively correlated to trusting beliefs in trusting intention in mobile telecommunication provider

P6: Trusting beliefs in telecommunication provider is positively correlated to trusting intention in mobile banking adoption

Table 2: Definition for Mobile Telecommunication Provider Trust Constructs

Mobile Banking Provider

Mobile banking provider refers to the retail banks or financial institutions that provide the mobile banking services. According to Gimun et al. (2009), mobile banking provider enables customers to access their bank account through mobile devices to conduct conventional and more advanced financial transactions. As technological innovation was found to be one of the ways to achieve competitive advantages, it is not surprising then that the Malaysian banking institutions are competing with each other to embrace their mobile banking services. For example, Standard Chartered claimed to be the first bank that applies smart-phone technology for mobile banking in the early year of 2007. Subsequently, Maybank declares that it is Malaysia’s first financial institution launching mobile banking application – M2UMap using iPhone. Most recently, Bank Islam launched another ‘first truly banking service’ in 2010 in which it enables users to perform their banking transactions anywhere and anytime without Internet connection (Cheah et al., 2011). Mobile banking can contribute to the banking industry by serving as a source of revenue, an additional distribution channel, and as an image-enhancing product. Mobile banking is complex and dynamic because there are many role-players (e.g. providers, content partners, customers and investors) in the development process (Dian, 2008). Lee & Chung (2009) showed that customers rated information quality, systems quality and the interface design quality provided by the mobile banking provider as critical in establishing their trust in mobile banking. A recent study has also indicated the importance of information quality and service quality provided by the mobile banking provider in developing initial trust in mobile banking (Zhou, 2011). The indicators of information quality include completeness, accuracy, format and currency. The indicators of systems quality include reliability, flexibility, integration, accessibility and timeliness. Other studies have also evidently showed that trust in mobile banking provider is important for mobile banking trusting intention (Meng et al., 2008; Min et al., 2008). Thus, based on McKnight et al. (2002) and supported by the aforementioned empirical evidences, the following prepositions are developed.

P7: Mobile banking provider trust is positively correlated to trusting beliefs in mobile telecommunication provider

P8: Mobile banking provider trust is positively correlated to trusting beliefs in trusting intention in mobile telecommunication provider

P9: Trusting beliefs in mobile banking provider is positively correlated to trusting intention in mobile banking adoption

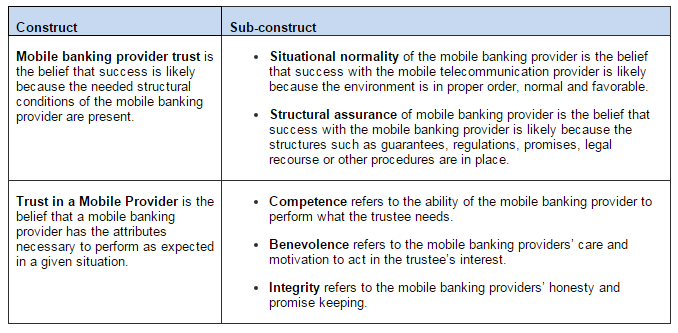

The definition for constructs and sub-constructs of the mobile banking provider trust is given in Table 3.

Table 3: Definition for Mobile Banking Provider Constructs

Conclusion

The intent of this paper has been to develop a conceptual framework on trust establishment in mobile banking. The framework indicates that three categories of trustees, which are the mobile banking provider, mobile telecommunication provider and the mobile technology are critical in establishing consumer trust leading towards mobile banking adoption. Based on the framework, several corresponding hypotheses were posited. The developed framework would be useful especially for researchers interested in investigating the topic. The survey research method would be the best option to help validate the framework and test the research hypotheses.

Acknowledgement

The authors would like to express their gratitude and appreciation to Accounting Research Institute, Universiti Teknologi MARA for funding the research.

References

Bangens, L. & Soderberg, B. (2008). ‘Mobile Banking: Financial Services for the Unbanked?,’ The Swedish Program for ICT in Developing Countries.

Google Scholar

Barnes, S. J. & Corbitt, B. (2003). “Mobile Banking: Concept and Potential,” International Journal of Mobile Communications, 1, 273-288.

Publisher – Google Scholar

Belanger, F. & Carter, L. (2008). “Trust and Risk in E-Government Adoption,” Journal of Strategic Information Systems17, 165—176.

Publisher – Google Scholar

Beng, T. C. & Eze, U. C. (2010). “Determinants of Mobile Payment Usage in Malaysia: A Conceptual Framework,”Journal of Electronic Banking Systems. [Online], [Retrieved January 21, 2012]

https://ibimapublishing.org/journals/JEBS/JEBS.html

Publisher

Central Bank of Malaysia (2012). List of Regulatees, [Online], [Retrieved January 21, 2012]

http://www.bnm.gov.my/microsites/payment/05_regulatees.htm

Publisher

Cheah, C. M., Teo, A. C., Sim, J. J., Oon, K. H. & Tan, B. I. (2011). “Factors Affecting Malaysian Mobile Banking Adoption: An Empirical Analysis,” International Journal of Network and Mobile Technologies. 2(3).

Publisher – Google Scholar

Daud, M. N., Kassim, N. E. M., Wan Mohd Said, W. S. R, & Noor, M. M. M. (2011). “Determining Critical Success Factors of Mobile Banking Adoption in Malaysia,” Australian Journal of Basic and Applied Sciences, 5(9): 252-265.

Publisher – Google Scholar

DeLone W. H. & McLean E. R. (1992). “Information Systems Success: The Quest for the Dependent Variable,”Information Systems Research, 3(1), 60—95.

Publisher – Google Scholar

Dobing, B. R. (1993). “Building Trust in User-Analyst Relationships,” Unpublished doctoral dissertation, Carlson School of Management, University of Minnesota.

Publisher – Google Scholar

Drexelius, K. & Herzig, M. (2001). ‘Mobile Banking and Mobile Brokerage — Successful Applications of Mobile Business?,’ International management & Consulting, 16(2), 20-23.

Eze, U. C. et al. (2008). ‘Modeling User Trust and Mobile Payment Adoption: A Conceptual Framework,’ Communications of the IBIMA, 3, 224-231.

Gefen, D., Karahanna, E. & Straub, D. W. (2003). “Inexperience and Experience with Online Stores: The Importance of TAM and Trust,” IEEE Transactions on Engineering Management, 50(3), 307—321.

Publisher – Google Scholar – British Library Direct

Gemalto (2011). “Mobile Banking: Product Overview,” [Online],[Retrieved January 21, 2012] http://www.gemalto.com/brochures/download/mob_banking_product.pdf

Publisher

Gimun, K. et al. (2009). ‘Understanding Dynamics between Initial Trust And Usage Intentions of Mobile Banking,’ Info System Journal. 19(3).

Goswami, D. & Raghavendran, S. (2009). “Mobile-Banking: Can Elephants and Hippos Tango?,” Journal of Business Strategy, 30(1), 14-20.

Publisher – Google Scholar

Gu, J.- C., Lee, S.- C. & Suh, Y.- H. (2009). “Determinants of Behavioral Intention to Mobile Banking,” Expert Systems with Applications, 36, 11605—11616.

Publisher – Google Scholar

InfoGile Technologies (2007). “Mobile Banking: The Future,” [Online],[Retrieved January 21, 2012]

www.infogile.com/pdf/Mobile_Banking.pdf

Publisher

InMobi (2011). “Media Impact on Media Consumption in Malaysia,” [Online],[Retrieved February 17, 2012] www.inmobi.com/research/consumer-research-2/

Publisher

Kim, G., Shin, B. & Lee, H. G. (2009). “Understanding Dynamics between Initial Trust and Usage Intentions of Mobile Banking,” Information Systems Journal, 19(3), 283—311.

Publisher – Google Scholar

Koo, C. & Wati, Y. (2010). “Toward an Understanding of the Mediating Role of Trust in Mobile Banking Service: An Empirical Test of Indonesia Case,” Journal of Universal Computer Science, 16(13), 1801-1824.

Publisher – Google Scholar

Lee, K. C. & Chung, N. (2009). “Understanding Factors Affecting Trust in and Satisfaction with Mobile Banking in Korea: A Modified DeLone and McLean’s Model Perspective,” Interacting with Computers, 21(5), 85—392.

Publisher – Google Scholar

Lin, H.- F. (2011). “An Empirical Investigation of Mobile Banking Adoption: The Effect Of Innovation Attributes and Knowledge-Based Trust,” International Journal of Information Management, 31, 252—260.

Publisher – Google Scholar

Liou, D. Y. (2008). “Four-Scenario Analysis for Mobile Banking Development Contextualized to Taiwan,” PICMET 2008 Proceeding, Cape Town, South Africa, July 27-31, 2008.

Publisher – Google Scholar

Lippert, S. K. & Davis, M. (2006). “A Conceptual Model Integrating Trust into Planned Change Activities to Enhance Technology Adoption Behavior,” Journal of Information Science, 32(5), 434-448.

Publisher – Google Scholar – British Library Direct

Li, X., Hess, T. J. & Valacich, J. S. (2008). “Why Do We Trust New Technology? A Study of Initial Trust Formation with Organizational Information Systems,” Journal of Strategic Information Systems, 17, 39-71.

Publisher – Google Scholar

Lu, Y., Yang, S. & Chau, P. Y. K. & Cao, Y. (2011). “Dynamics between the Trust Transfer Process and Intention to Use Mobile Payment Service: A Cross Environment Perspective,” Information & Management, 48, 393-403.

Publisher – Google Scholar

McKnight, D. H., Carter, M., Thatcher, J. B. & Clay, P. F. (2011). “Trust in a Specific Technology: An Investigation of its Components and Measures,” ACM Transactions on Management Information Systems, 2(2).

Publisher – Google Scholar

McKnight, D. H. & Chervany, N. L. (2002). “What Trust Means in E-Commerce Customer Relationship: An Interdisciplinary Conceptual Typology,” International Journal of Electronic Commerce, 6(2), 35-59.

Publisher

McKnight, D. H., Choudhury, V. & Kacmar, C. (2002). “Developing and Validating Trust Measures for E-Commerce: An Integrative Typology,” Information Systems Research, 13(3), 334-359.

Publisher – Google Scholar – British Library Direct

Meng, D., Min, Q. & Li, Y. (2008). “Study on Trust in Mobile Commerce Adoption: A Conceptual Framework,” Proceedings of the 2008 International Symposium on Electronic Commerce and Security, Ghuangzhou City, China, August 3- 5, 2008.

Publisher – Google Scholar

Min, Q, Meng, D. & Zhong, Q. (2008). “An Empirical Study on Trust in Mobile Commerce Adoption,” Proceeding of the2008 IEEE International Conference on Service Operations and Logistics, and Informatics, Beijing China, October 12-15, 2008.

Publisher – Google Scholar

Rahman, S., Haque, A. & Ahmad, M. I. S (2011). “Choice Criteria for Mobile Telecom Operator: Empirical Investigation among Malaysian Customers,” International Management Review, 7(1), 50-51.

Publisher – Google Scholar

Sharma, N. & Ojha, S. (2004). “Measuring Service Performance in Mobile Communications,” The Service Industries Journal, 24(6): 109-128.

Publisher – Google Scholar – British Library Direct

Soderstrom, E. (2009). “Trust Types: An Overview,” Proceedings of the 8th Annual Security Conference Discourses in Security Assurance & Privacy Las Vegas, NV, USA April 15-16, 2009.

Publisher – Google Scholar

Woo, K.- S. & Fock, H. K. Y. (1999). “Customer Satisfaction in Hong Kong Mobile Industry,” The Service Industries Journal, 19(3): 162-174.

Publisher – Google Scholar – British Library Direct

Zhou, T. (2011). “An Empirical Examination of Initial Trust in Mobile Banking,” Internet Research, 21(5), 527-540.

Publisher – Google Scholar